Weekly Notes from Tim

By Tim Holland, CFA, Chief Investment Officer

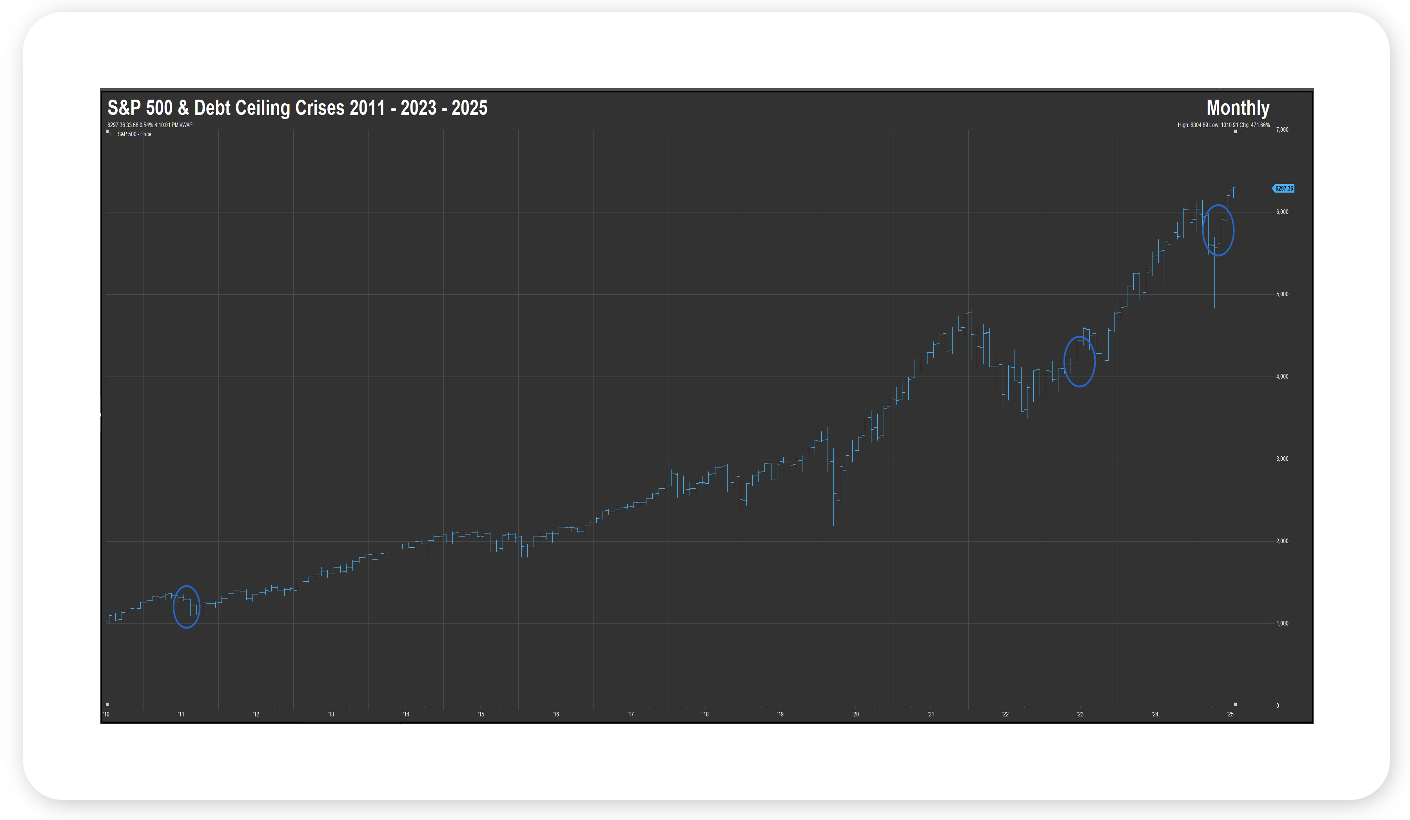

- Much of the reporting on The One Big Beautiful Bill Act has focused on its impact on the tax code and its potential impact on US deficits and total debt, and understandably so – how much money companies and consumers have to spend, and the fiscal health of the US are big issues. That said, we think The OBBBA’s raising of the US debt ceiling by $5 trillion (from $36 trillion to $41.1 trillion) is also pretty important and worthy of a bit more attention.

- As you know, the US debt ceiling, which serves as a cap on how much money the Federal Government can borrow, has on more than one occasion been a source of concern for Wall Street, as the Federal Government bumps up against it, our political representatives in Washington, DC can’t agree to raise it, and the ability of the US to pay its bills gets called into question (and, more ominously, talk turns to a potential US debt default). By one count, there have been 10 US debt ceiling crises over the past 15 years, where the US government has come very close to running out of money, with the crises of 2011, 2023 and 2025 serving as key catalysts for the US losing its three AAA credit ratings. That said, while US stocks might have wobbled during those and other debt ceiling crises since 2010 (see chart), they have always found their footing and gone onto make new highs – and the US government has always gone onto raise the debt ceiling.

- Agree or disagree with the fiscal policy path President Trump and Congressional Republicans have chosen, we do see The OBBBA becoming law as a net positive for investors near-term, increasing the odds that the US economy continues to expand and that US equities continue to catch a bid into 2026, with reasons for that thinking including the policy certainty the bill’s passage creates; current tax rates remaining in place; incremental tax cuts tied to tips and overtime income, and incentives for companies to invest in productive assets. Most policy experts think the US won’t bump up against its $41.1 trillion debt ceiling until sometime in 2027, making the debt ceiling one less thing for Wall Street to worry about, at least for now.

Data Source: FactSet, 7/17/2025

Looking Back, Looking Ahead

By Ben Vaske, BFA, Manager, Investment Strategy

Last Week

Markets moved modestly higher last week, led by tech. The NASDAQ 100 gained over 1% and now leads the S&P 500 by nearly 2.5% YTD. Value stocks and blue chips slipped, while developed international markets continue to lead domestic YTD, and continue to close the gap with the S&P 500 over longer time frames. The US dollar strengthened for the second week in a row, gaining over 1%, and trimming its earlier double-digit YTD decline.

Economic data came in broadly supportive of the “healthy economy” narrative. June CPI rose 0.3% month-over-month and 2.7% year-over-year, in line with expectations. While headline numbers showed progress, underlying inflation dynamics are being closely watched, especially with tariffs potentially pushing up goods prices later this year.

Retail sales surprised to the upside, rising 0.6% in June after back-to-back declines in April and May. Including revisions, the gain was closer to 0.7%. Consumer spending is showing resilience, particularly in goods-heavy categories. With consumption driving ~70% of US GDP, this rebound is an encouraging sign for economic momentum.

Q2 earnings kicked off their first full week, with early results led by Financials. FactSet reports that 83% of reporting S&P 500 companies have posted positive EPS and revenue surprises. The blended earnings growth rate for the quarter sits at 5.6%, which would mark the slowest pace since Q4 2023.

This Week

Earnings season hits a key stretch, with Tesla and Alphabet set to report alongside several Communication Services names that beat expectations last quarter. On the economic calendar, new home sales, leading indicators, and PMI data are due. May's new home sales report showed a 13.7% drop, the largest since mid-2022, so follow-through will be closely watched amid a struggling housing market.

The Fed meets next week on July 30th, and markets are assigning a 96% probability of no change. Odds of two rate cuts by year-end remain on the table, though they’ve softened slightly in recent weeks.

We hope you have a great week. If there’s anything we can do to help you, please feel free to reach out to ben.vaske@orion.com or opsresearch@orion.com.