Our investment team is closely monitoring the developments in the Middle East and the impact they are having on commodity prices, the stock market, and the world economy. We lament the loss of innocent life, pray for the safety of U.S. troops in harm’s way and mourn the U.S. military servicemembers who have lost their lives.

You will continue to hear from us on the conflict with Iran. In the meantime, if you have any questions on the markets and the economy or if there is anything we can do to support you and your clients during this difficult time, please reach out to us via our Investment Strategy Team’s email address at opsresearch@orion.com.

Weekly Notes from Tim

By Tim Holland, CFA, Chief Investment Officer

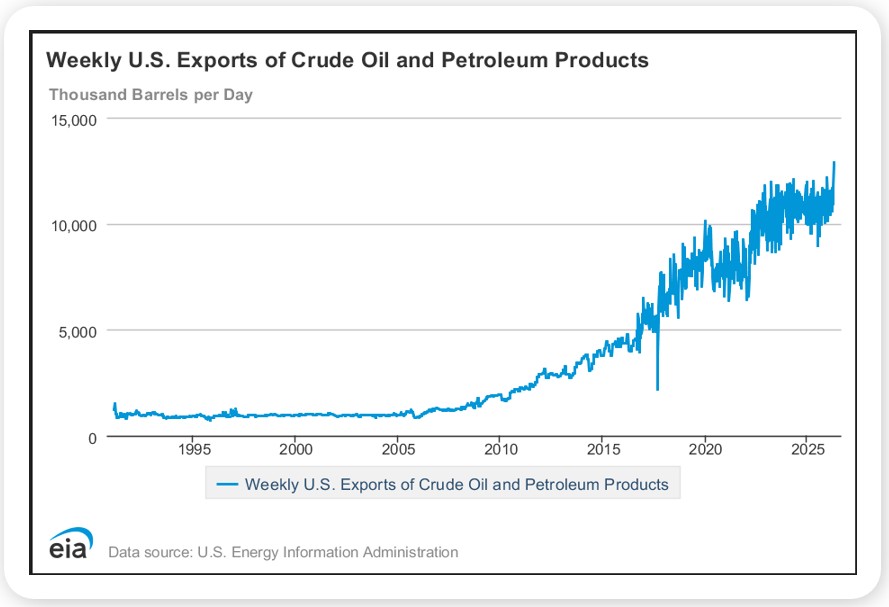

- We have written often about the remarkable impact hydraulic fracturing or “fracking” has had on America’s energy profile, about how the U.S. went from pumping 4.7 million barrels of oil a day in 2008 to pumping 13.8 million barrels of oil a day in 2025; about how the U.S. went from being a net importer of 13 million barrels of oil and petroleum products a day in 2005 to being a net exporter of 3.8 million barrels of oil and petroleum products a day in 2025, and about how the US went from being a net importer of 3.8 trillion cubic feet of natural gas in 2007 to being a net exporter of 5.7 trillion cubic feet of natural gas in 2025.

- America’s evolved energy profile would be a big deal for our economy, national security and international standing at any point in time; it strikes us as a particularly big deal given the war in the Middle East and the closing of the Strait of Hormuz, the waterway through which 20 million barrels of oil used to travel daily, or roughly 25% of all seaborne oil trade, mostly destined for markets in Asia. And as access to Middle Eastern oil is curtailed, the world is turning to U.S. oil to meet its energy needs. More specifically, according to the U.S. Energy Information Administration, in mid-April U.S. oil exports hit a record 12.9 million barrels a day (see chart). While it is unlikely that U.S. energy companies will hold onto all their recent market share gains as the war winds down, it is likely they will hold onto some of those market share gains, giving the U.S. a more prominent role in global energy markets going forward.

- We were all aware of our country’s economic and geo-political advantages before the war with Iran….the U.S. as home to the world’s largest economy, the world’s largest and most liquid equity and fixed income markets and the world’s most powerful military; the U.S. with oceans on either side of it and friendly neighbors above and below it; a U.S. economy driven by domestic consumption and not external demand; the U.S. as the printer of the world’s reserve currency and the U.S. as the world’s leading producer of oil and natural gas. The war has only amplified those advantages we think, particularly as it concerns energy.

Source, U.S. Energy Information Administration, April 2026

Looking Back, Looking Ahead

By Ben Vaske, BFA, Manager, Investment Strategy

Last Week

Markets extended their recent run of strength last week, with the S&P 500, NASDAQ, and Dow all reaching new all-time highs and the S&P 500 posting a gain of roughly 1% on the week. The S&P 500 and NASDAQ 100 have now been positive for five consecutive weeks and sit up 6% and 10% year-to-date, respectively, despite a challenging start to the year. The broader rally over the last three years has delivered exceptional returns for balanced, diversified investors, led by U.S. technology stocks.

Earnings season was a major driver of sentiment, as blowout results from several Magnificent 7 names sent Q1 earnings growth estimates surging to 27% year-over-year, which would be the strongest pace of growth since Q4 2021. With 63% of S&P 500 companies having reported, 84% have beaten earnings expectations and 81% have topped revenue estimates. On the economic front, data was mixed: GDP came in slightly below expectations at 2.0% annualized growth, PCE inflation ticked higher to 3.5% year-over-year, and the Fed held interest rates steady at its April meeting amid the highest level of internal dissent in decades.

Performance across asset classes was broadly constructive. Interest rates edged slightly higher, keeping the Bloomberg Agg close to flat on the year, and the U.S. dollar fell sharply for the second consecutive week, providing a tailwind to developed international equities. Emerging markets remain the top-performing equity class in 2026.

This Week

Employment data takes center stage this week, with ADP on Wednesday and the government's jobs report on Friday. Current expectations call for roughly 53,000 jobs added and no change to the unemployment rate at 4.3%. Earnings season remains active as well as we continue through some of the heaviest weeks of this quarter’s releases. Notable names this week include Palantir, Advanced Micro Devices, and a number of software companies.

We hope you have a great week. If there’s anything we can do to help you, please feel free to reach out to ben.vaske@orion.com or opsresearch@orion.com.