The stock market is starting the week with slightly lower prices, as interest rates continue to move higher. The 10-year Treasury yield hit 2.87% this morning, its highest level since 2018 and nearing 2x the level at the end of last year (CNBC, April 2022).

This week ahead is loaded with earnings reports from a variety of economic sectors. This will likely be the primary source of price action this week.

The US stock market slipped again last week. In terms of returns last week, the overall US market was down about 2% (CNBC, April 2022). International stocks, however, were slightly higher. Value outperformed growth by 2% last week (CNBC, April 2022).

Among Diversifiers, the overall investment-grade bond market lost about 1%, but Alternatives and Commodities were both up over 1% (Yahoo Finance, April 2022).

For the year, the US stock market is now down -8% (CNBC, April 2022). Despite a rising US dollar, non-US stocks are also down about 8% (CNBC, April 2022).

US Growth stocks are now down -19% year-to-date, while US Value stocks are up nearly +3% (Yahoo Finance, April 2022).

Regarding year-to-date performance among Diversifiers, the overall investment-grade bond market (defined by Bloomberg US Aggregate Index) is now down a whopping 9%, with Alternatives (defined by Morningstar Diversified Alternatives Index) up +2% and Commodities (Bloomberg Commodity Index) higher by a sizzling +34% year-to-date return.

In my experience, 3-year returns, especially 3-year relative performance numbers, drive a lot of investment flows. Well, we just had an important change in some 3-year relative performance numbers: commodities are now up by about 18% per year over the last 3 years while US Stocks are now “only” up 16%. It should be noted that US Growth stocks are still up by slightly more than 18%.

Again,Ten Year Treasury Yields rose last week, closing at 2.83% (up 12 basis points from the week before) (Yahoo Finance, April 2022).

We know it was an awful quarter for Treasury bonds, but did you know that corporate bonds did even worse and had theirworst quarter since 1980?

Never mind the actual stock market return numbers, there were some really big sentiment numbers last week – some of the worst in decades. And I believe that those numbers are a call for action for all of us.

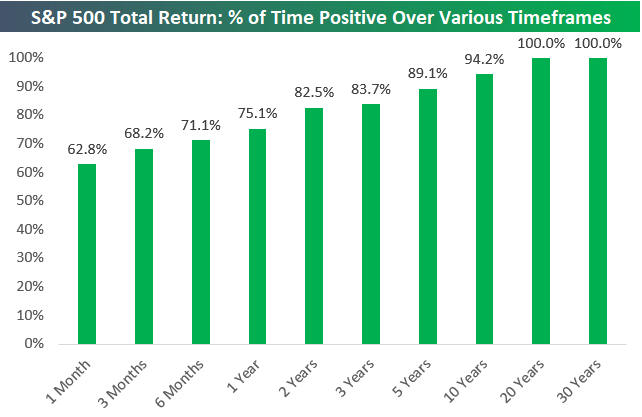

According to the AAII Investor Sentiment Survey, the level of bullish investors (i.e., positive outlook for the next 6 months) is the lowest since 1992! Think about this. Not even the dot.com Crash, the Financial Crisis, or the recent pandemic created such a low level of enthusiasm for stocks than right now. Those were three epic bear markets. We are now only 5% off the all-time highs. By the way, the market is up 71% of the time over6-month periods according to Bespoke Investments. Also, when sentiment is this poor, the stock market has historically produced above-average returns in the following week, month, 3-, 6-, and 12-months later.

It’s just not individual investors, but professional portfolio managers arethe most gloomy ever.

And, as mentioned last week, according to theBespoke Consumer Pulse survey report of American consumers, only three demographic categories (incomes of $100k-$150k, those aged 25-34, and those aged 35-44) reported net economic sentiment above the bottom 10% of readings historically, and only two categories have a net positive economic sentiment reading (Income: $100k-$200k and Personal Finances: Positive). Overall, a net 33.5% of respondents view the economy negatively. The bottom line, people are super negative about the economy right now. What’s the leading driver of the negative sentiment: inflation?

In my opinion, as investment professionals whose mission is to help investors reach their financial goals, this is the time when we really need to step up and fulfill that calling. For us, this is an important time. It’s when we earn our keep. Investors need our counsel. Our education and encouragement on how markets should/could behave. Why their investment plans are appropriate. All of our training and experience were to prepare us for times like these.

Some big numbers from economic news last week. A few bullets:

The Bureau of Labor Statistics (BLS) Consumer Price Index (CPI) rose 8.5% in March compared to the same month last year, according to the latest report released Tuesday. That marked thefastest rise since 1981.

The Producer Price Index (PPI) rose 1.4% in March, coming in above the consensus expected +1.1%. Producer prices areup 11.2% versus a year ago.

Let’s break down some quick good and bad points from the latest inflation numbers. Let’s get it from “The Inflation Guy” (who we interviewed this past week for The Weighing Machine podcast. The interview will be published several weeks from now).

First, the good news. I expect today's figures will mark the highs for the year. The comps get hard hereafter: in April 2021, Core CPI rose 0.86% month-over-month, 0.75% in May, and 0.80% in June.

The bad news is that inflation might not ebb very far. The last 5 monthly core prints have been between 0.5% and 0.6%. The central tendency of the distribution appears to have moved up from 2-3% to maybe as high as 6%+.

One final word - 75% of the weight in the CPI is now inflating faster than 4%. More than a third of the basket is inflating faster than 6%.

By the way, the “Inflation Guy” had one of myfavorite economic podcasts last year, where he cleverly interviewed Milton Friedman last December. Oh, Friedman passed away nearly 20 years ago.

You’ve surely heard and read how mortgage rates are screaming higher, right? Well, they are clearly moving sharply higher, but here’s the history:50 Years of 30-Year Fixed Mortgage Rates from the St. Louis Fed. In short, mortgage rates are still low. And remember that’s in nominal terms. Adjust for inflation, and rates are still attractive.

Given the rise in mortgage rates, many are becoming worried about housing. In a piece by First Trust, they say housing will likely getheartburn, not a heart attack. In short, they argue that while 5% mortgage rates are high relative to where they recently were, home prices should still rise 5 - 10% this year, meaning home prices either keep up with or exceed borrowing costs. Real mortgage rates (the rate minus inflation) are still negative.

One more quick tidbit from the aforementioned First Trust article, and a good counterpoint to those concerned about an inverted yield curve. “Negative real rates are also why we are not yet worried about an inverted yield curve from the 2-year Treasury to the 10-year. In the past, when inverted yield curves preceded recessions, real interest rates were positive, not negative.” Excellent point.

Not everything in fixed income looks terrible. The “Inflation Guy” also mentioned this in the interview and even the WSJ had this article last week:The Safe Investment That Will Soon Yield Almost 10%. In short, “Series I Bonds” are very hot right now, and for good reason. Though it’s not an investment for institutional investors (you can only invest $10k/year into them), many investors should consider them.

More on Series I Bonds and a hat tip to Ben Carlson for this nice overview:How Series I Savings Bonds Work overview. Ben’s words (but also the words of many others right now): “You will not find a better deal in fixed income right now.”

You buy these bonds straight from the government at Treasury Direct.

The yield is computed every 6 months (in May and November) and compounds semi-annually.

There is a fixed component (which is currently 0%) and an inflation-indexed component tied to CPI that resets semi-annually.

There is a $10,000 limit per person (you can buy them for your kids too) annually.

If you send your tax refund directly to Treasury Direct, you can buy an extra $5,000 per year.

You don’t pay any state taxes and federal income tax can be deferred until redemption.

If you use these bonds to pay for education expenses, they are tax-free.

You cannot cash in these bonds in the first 12 months.

If you cash in before 5 years is up, you pay a penalty of 3 months’ worth of interest.

After 5 years you can redeem penalty-free.

There is a lot of housing data in the first three days ofthis week's economic calendar. Federal Reserve Chairman Jerome Powell is publicly talking Thursday.

The Atlanta Fed’sGDPNow estimate for 1Q growth is now 1.1%. This is unchanged from the week before.

Earnings season is off to a decent start with 77% of S&P 500 companies reporting earnings per share above expectations according toFactset

That said, only 7% of companies have reported so far. Currently, the consensus is that first-quarter earnings will jump 5% for the quarter, but given that actual earnings typically beat estimates, it’s very reasonable to expect 10%+ earnings growth when it’s all said and done.

There’s new stuff coming up in the quarterlyOPS Reference Guide, including how often we see year-over-year real GDP growth at certain levels over time.

Currently, real GDP year-over-year growth at the end of last year was 5.5%.

What might be a bit surprising, however, is that while earnings growth still averages double-digit growth during times of strong GDP growth, earnings growth is actually lower than it is when GDP growth is a bit lower (like when it is 2-3% year-over-year). This, however, is consistent with other studies that show that GDP growth is not strongly correlated with stock market performance.

Crypto Corner – Grant Engelbart, CFA, CAIA, Brinker Capital Sr. Portfolio Manager

Cryptocurrencies struggled again last week, with Bitcoin falling -7% to just over $40k. Ethereum dropped nearly -8%. Most other major coins fell 8-12%.

Circle, a crypto payments company, received $400 million in funding led by BlackRock, who will also manage the dollar assets that back Circles Stablecoin. President Biden appointed Michael Barr to become Vice President of Supervision at the Federal Reserve. Barr was a former advisor to cryptocurrency firm Ripple Labs.

Digital Asset ETF news was light last week, but despite a lackluster performance in the space as of late, interest is still very high amongst the ETF community.

Additional Resources

Speaking of crypto, this week onOrion's The Weighing Machine podcast we interview Chris King from Eaglebrook Advisors, a leading Bitcoin and crypto SMA platform. Want to learn some of the basics behind crypto, what’s driving price action of late, and what the future might hold for this asset class? Check out the podcast!

This month’sMonthly Portfolio Recipe Webinar is “Core and Explore” and is a nice contrast in styles, in terms of both investment approach and presentations, with Janus Henderson and Howard Capital. Our upcoming speakers from Janus Henderson are Ash Alankar the highly regarded Head of Global Asset Allocation and the legendaryMyron Scholes. From Howard Capital, we have the widely liked Vance Howard.

Speaking of trips to Omaha, here is the schedule for the College World Series for NCAA baseball. C’mon out!

Thanks for reading and have a great week! For more resources, please check out theFinancial Advisor Success Hub, and as always, please let us know what we can do better at rusty@orion.com or ben.vaske@orion.com.

For financial advisors to get the Monday Morning Market Insights (aka “Monday Morning Bullets”) delivered straight to their inbox, visit to linkSubscribe to Weekly Bullets.

Have a great week! Invest well and be well.

The CFA is a globally respected, graduate-level investment credential established in 1962 and awarded by CFA Institute — the largest global association of investment professionals. To learn more about the CFA charter, visit www.cfainstitute.org.

The CMT Program demonstrates mastery of a core body of knowledge of investment risk in portfolio management. The Chartered Market Technician® (CMT) designation marks the highest education within the discipline and is the preeminent designation for practitioners of technical analysis worldwide. To learn more about the CMT, visit https://cmtassociation.org/.

"The CAIA® is the globally-recognized credential for professionals managing, analyzing, distributing, or regulating alternative investments. To learn more about the CAIA, visit https://caia.org/."

{kind=link}