Key Takeaways:

- Markets entered 2026 pricing roughly two Fed rate cuts but now assign an 85% chance of at least one rate hike by year end.

- New Fed Chair Kevin Warsh's first meeting marked a substantive shift in how the central bank operates, including a shortened policy statement, the elimination of forward guidance, and committee projections showing nine officials expecting at least one hike this year.

- Because the inflation surge is largely supply-driven, the path forward remains highly scenario-dependent: a durable Iran peace agreement could unwind hike expectations as quickly as they formed, reinforcing that rate expectations are a snapshot of sentiment rather than a schedule of events.

Few dynamics in markets illustrate the limits of forecasting quite like the evolution of Federal Reserve policy expectations over the first half of 2026. Entering the year, futures markets were pricing in roughly two rate cuts by the end of this year, and the Fed's own December projections pointed toward continued easing. Today, markets assign roughly 85% odds that the Federal Reserve raises rates by its December meeting. A shift of this magnitude in six months is rare, and understanding its drivers offers a useful lens on both the current policy environment and the nature of market expectations more broadly.

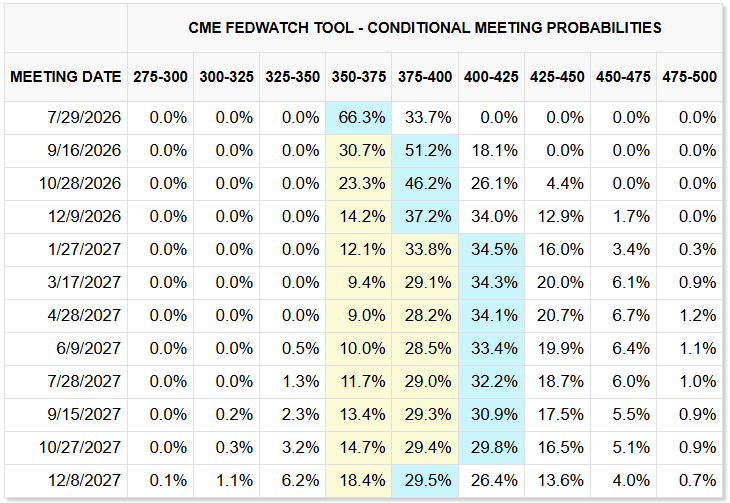

Source: CME FedWatch, 7/13/2026

Since the conflict with Iran began in late February, elevated energy prices have pushed headline CPI to 4.2% year over year (as of the May release), the highest reading since April 2023 and more than double the Federal Reserve's 2% target. Critically, this episode is largely a case of supply-shock inflation, meaning price pressure driven by disruptions to the supply of goods, in this instance oil, rather than by excess demand. Supply driven inflation is a more complex issue for the Federal Reserve. Rather than the typical “overheating” of demand that drives inflation, supply shocks are generally caused by exogenous events that tightening monetary policy provides less impactful remediation. Central banks have historically been more inclined to look through supply-driven episodes, as higher interest rates do little to reopen a shipping lane or restore lost production. Consistent with that framework, core inflation measures excluding food and energy have risen far more modestly, which helps explain why the Fed has remained on hold rather than tightening already.

The labor market has complicated rather than clarified the picture. May payrolls surprised to the upside at 172,000 with unemployment holding at 4.3%, weakening the case for cuts. June payrolls then registered a soft 57,000, including sharp downward revisions to previous months, muddying the case for hikes. With each release pointing in a different direction, it is of little surprise that market-implied probabilities have been repricing continuously.

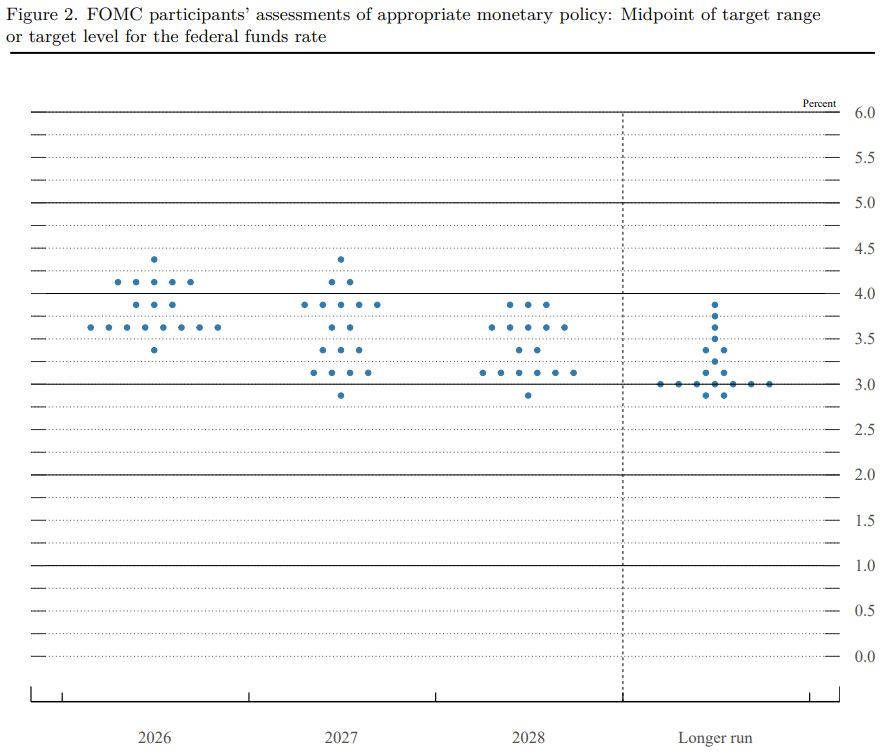

On top of a complicated data-drawn picture, Kevin Warsh assumed the chairmanship from Jerome Powell in May, and his first policy meeting in June demonstrated that the "regime change" was more than political posturing. The committee held its target range steady at 3.50% to 3.75%, but the substance surrounding that decision changed considerably: a dramatically shortened policy statement, the removal of language leaning toward future cuts, the elimination of forward guidance altogether, and the creation of five internal task forces charged with reviewing areas ranging from Fed communications to the inflation framework itself. Most notably, the committee's projections erased the prior expectation for a cut this year, with nine officials indicating at least one hike before year end and only a single participant still projecting a cut in 2026. Warsh declined to submit his own projection, consistent with his longstanding skepticism of forward guidance, though his press conference remarks on delivering price stability were direct enough that the probability of a September hike nearly doubled in a single day following the June meeting.

Summary of Economic Projections, Federal Reserve, 6/17/2026

Looking ahead, markets overwhelmingly expect another hold at the July 29 meeting, but the path from there splits into two main plausible scenarios. Should the Strait of Hormuz continue on a path of reopening, energy prices could continue retracing, headline inflation could converge toward core readings, and the hike currently priced for December could dissipate as quickly as the cuts did this spring. Should energy pressures persist or see their effect broaden into other categories, the committee has clearly signaled its willingness to act. Warsh has also introduced a longer-term consideration of his own, arguing that productivity gains from artificial intelligence should ultimately prove disinflationary, a view that may shape how patient the new regime at the FOMC proves to be.

The same futures market that confidently priced two cuts in January now prices at least one hike by December, and both readings reflected the best available information at the time. The Federal Reserve itself has stopped offering guidance on the future path of rates, an acknowledgment that no one, including the committee, knows that path with certainty. Rate expectations are a snapshot of sentiment, not a schedule of events. Positioning that depends on a single policy outcome has been penalized twice already this year, while positioning built to participate across a range of outcomes has weathered the repricing without incident.