The conflict with Iran sent shockwaves through the world and markets, and has required a large portion of investors’ attention. Our team has published our thoughts on the initial conflict and what it means for markets, as well as an update on oil prices and the investor outlook. We are mindful of the anxiety this is causing. There were, however, other important dynamics shaking out in markets before the conflict began that we believe will remain important for advisors to be familiar with going forward.

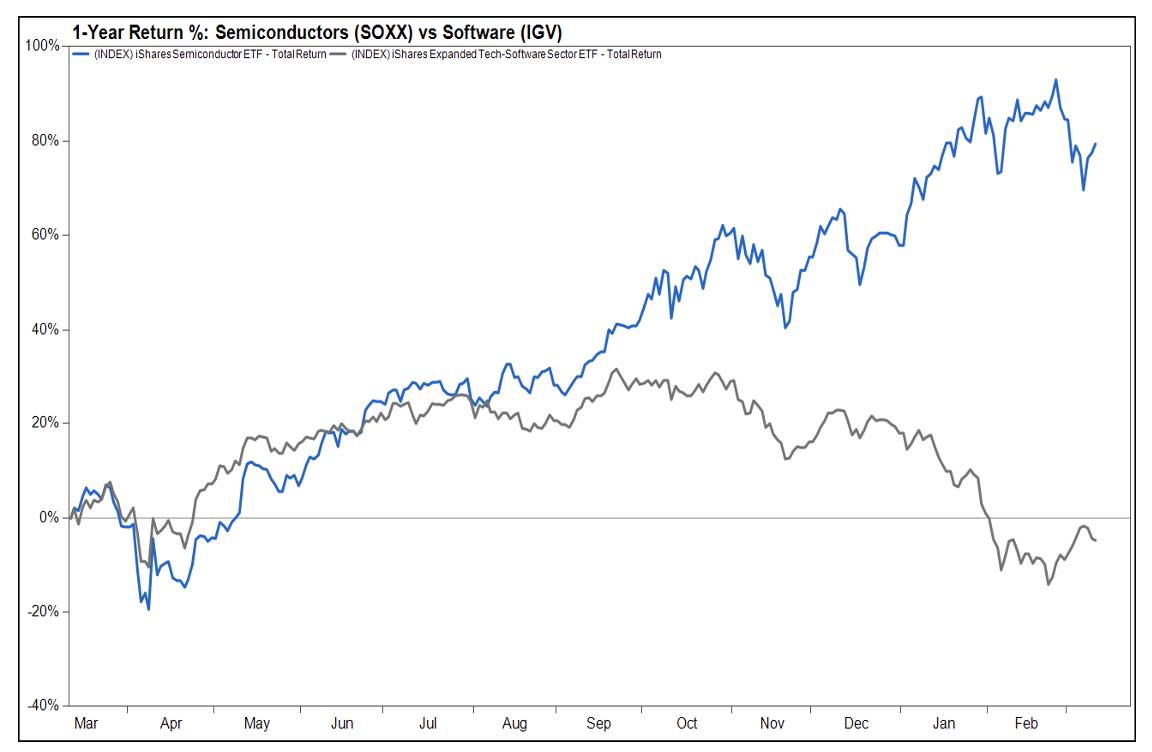

Software-as-a-service (SaaS) stocks began to struggle in late 2025, but the selloff accelerated sharply in late January and into February when Anthropic released Claude Cowork, a desktop agent that automates workflow across files and tasks. This tool, among other AI advancements in recent months, appeared to threaten the competitive advantages of some widely used SaaS products, and investors began to weigh the potential for AI to structurally disintermediate SaaS companies over the next few years. IGV, an ETF tracking the U.S. software industry, fell more than 20% in a matter of weeks and remains more than 25% off its September high as of this writing, despite a relative recovery from its late February lows. This shift notably marked a decoupling in performance between semiconductors (blue) and software (gray):

Source: FactSet, as of 3/10/2026

We know this market action has caused investors some anxiety about their U.S. tech exposures, and this is a topic we’ve been thinking about internally for some time. I was recently in New York City and had the chance to sit down with Maria Karahalis, Investment Director and Portfolio Strategy Manager at Capital Group, to discuss these developments in more detail. The rest of this piece includes key takeaways from that conversation, as well as our own thoughts, all designed to provide advisors with context and talking points for client conversations addressing some of the market’s primary concerns in this space.

Market Concern: AI-assisted coding (“vibe-coding”) allows companies to create their own software

- The bear case here is straightforward: if AI can generate functional, customized software from a plain-language prompt, the value proposition of off-the-shelf SaaS products would erode. Why pay ongoing subscription fees for a product built for the masses when you can build something tailored to your specific workflow in an afternoon? This concern is particularly acute for niche, single-function software products – tools that solve one specific problem and charge a recurring fee to do it. Those products are arguably the most vulnerable to being replicated by an AI agent with minimal technical oversight.

- Even though this may be possible, is this economical? For example, Maria pointed out that the basic subscription to Shopify costs $29/mo, and they have millions of customers. High quality software has low barriers to entry in lots of cases, and companies focused on growing their business may find it more cost effective to continue using robust software services instead of spending time and resources vibe coding their own software.

- Companies like Salesforce and ServiceNow are so embedded in their enterprises who have spent years and millions of dollars building out their tech stacks. That doesn’t mean they have permanent status, but companies are unlikely to rip out their software overnight in pursuit of creating their own. The focus may be more on integrating new technology with existing infrastructure rather than reinventing.

Market Concern: AI allows companies to be more productive with less employees, damaging software companies’ seat-based pricing models

- Most major SaaS companies (Salesforce, Workday, ServiceNow, etc.) charge customers based on the number of users accessing their platform. If AI agents can handle tasks previously performed by ten, twenty, or fifty employees, companies may reduce the headcount that interacts with these platforms. Even a modest reduction in seats across millions of enterprise contracts could translate into a significant revenue decline. The challenge for software companies is that pivoting away from seat-based pricing involves friction – repricing existing contracts, retraining sales teams, and rebuilding financial models around usage-based revenue is a long-term undertaking, and there could be meaningful revenue shortfalls in the interim.

- However, companies are projected to spend more on software in 2026, not less. A February report from Gartner estimates that $1.4 trillion will be spent on software in 2026, representing 15% growth from 2025. If anything, AI adoption may be driving new software purchases: security tools, AI management platforms, and cybersecurity software may help to offset potential seat losses elsewhere.

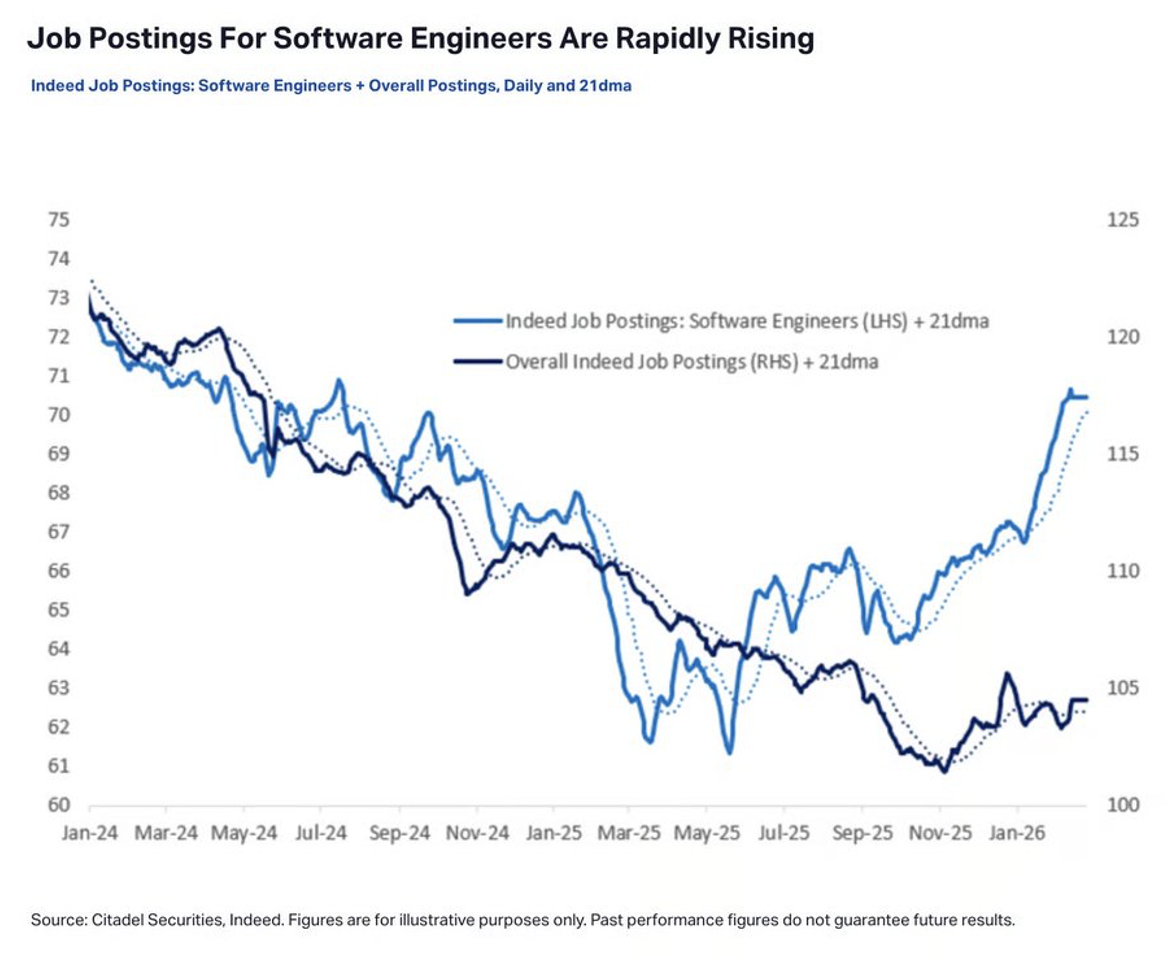

- The job displacement narrative may be a bit overblown. In fact, job postings on Indeed for software engineers are spiking:

Source: Daily Chartbook via X

Market Concern: Software companies are racing to create their own AI systems, but will be unable to keep pace with the advancements of the AI-native architectures (Claude, ChatGPT, etc.)

- Foundation model companies like Anthropic and OpenAI are building AI systems from the ground up, with reasoning and autonomy baked into their core design. Traditional software companies, by contrast, are retrofitting AI onto platforms built for a pre-AI world, and the worry is that gap compounds over time as foundation models iterate at a pace incumbents cannot match. The historical parallel that makes investors nervous is the cloud transition, when on-premise giants like Oracle and SAP scrambled to build cloud products while born-in-the-cloud companies like Salesforce outpaced them. The concern is that today's SaaS incumbents now find themselves in yesterday's on-premise vendors' shoes.

- However, today’s incumbents have advantages that the AI-natives don’t: proprietary data, distribution, customer relationships, and high switching costs. The data is enormously valuable for training AI models in a specific business context, and that isn’t something the AI-natives can replicate. The incumbents who leverage that data effectively could potentially build better domain-specific AI than the foundation model companies.

- It’s worth noting that Oracle and SAP remain enormous, profitable companies who adapted to the change they were faced with during the cloud transition. The transition created winners and losers in the incumbent category rather than wiping it out completely.

Key Takeaways

- There is genuine excitement about what this new technology is really going to be capable of. We’re in a period of change. Change can have businesses that wash out, but also allows companies to adapt and emerge better than before.

- The narrative of a broad-based “SaaS-pocalypse” is likely unfounded. There will be winners and losers across the ecosystem, and markets are still trying to parse out who is willing and able to adapt. This shakeout may take months or even years before the winners and losers become clear, potentially favoring active managers in the interim.

- The future of software is likely to look different than the past, but equity investors with long time horizons and a disciplined plan are more likely to benefit from this structural change than those who abandon the sector altogether.