Weekly Notes from Tim

By Tim Holland, CFA, Chief Investment Officer

- There is more than one way to build an equity index…you could take a geographical approach (country, region, or world); a style approach (growth or value); a size approach (small, medium, or large); a factor approach (momentum, yield, quality) or a sector approach (technology, materials, financials). But once you have identified the stocks you want in your index you must decide how to place them or weight them in your index – market cap, price or equal distribution.

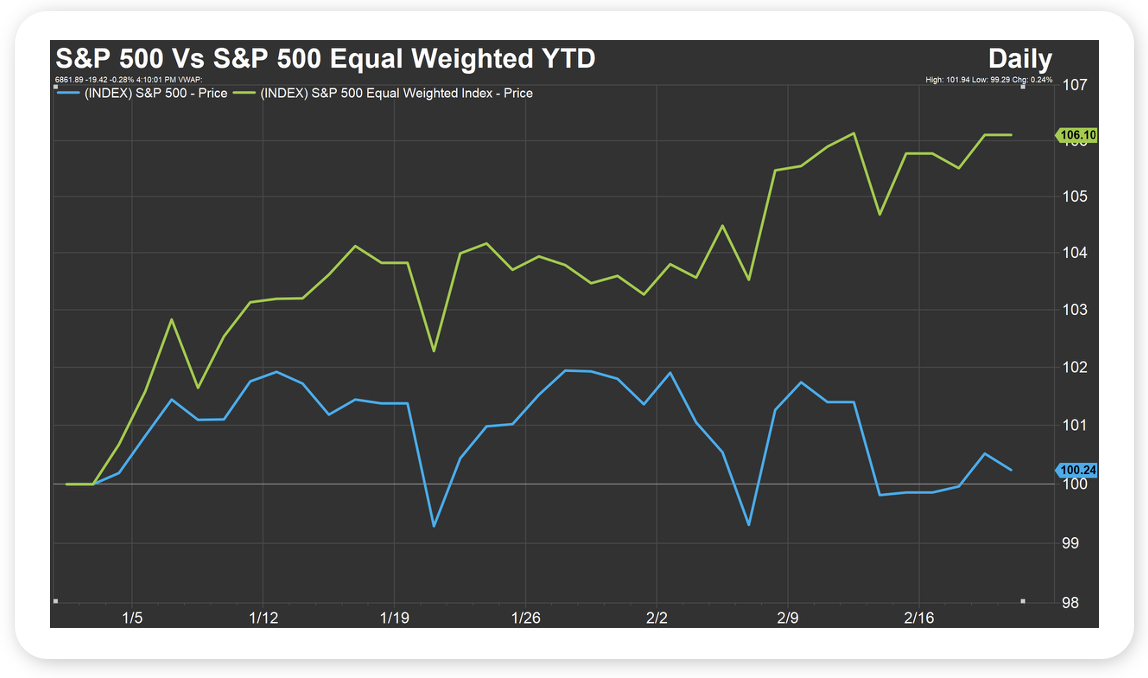

- The most famous index in the world – the S&P 500 – is made up of companies that share certain characteristics – including size and profitability – that are weighted by market cap, meaning the bigger the market cap (which as we know is really just the price of the stock times shares outstanding) the bigger the weight in the index (which is how the Magnificent 7 came to make up about 37% of the S&P 500 at their collective market cap peak). That index, as of February 19th, is up just 0.2% year to date, reflecting a meaningful rotation by investors out of US large cap technology stocks, including the Mag 7 (which still account for about 33% of the index), and into US value and US small cap stocks, which have performed much better of late on an absolute and relative basis.

- We have written why that rotation should prove to be a positive development for the market, as more companies catch a bid and the bull market broadens out, even as US large cap tech stocks stumble (six of the Magnificent 7 stocks are in the red for 2026 with only Nvidia positive, and by less than 1%). To put a finer point on the performance differential between large cap technology stocks and the rest of the market, the S&P 500 Equal Weighted Index is up 6.1% in 2026, outdistancing the better known, and better followed S&P 500 by 5.9% (see chart).

- Markets have been volatile in 2026, while the market’s bellwether index has done a whole lot of nothing, but if you look past the market cap weighted S&P 500 and focus on the equal weighted S&P 500, the performance story brightens considerably.

Source: FactSet, February 19, 2026

Looking Back, Looking Ahead

By Ben Vaske, BFA, Manager, Investment Strategy

Last Week

The biggest headline came from the Supreme Court, which struck down the administration’s use of emergency powers under IEEPA to impose sweeping global tariffs. While that ruling removed one policy lever, tariff pressure has not disappeared. The administration has since signaled it is exploring alternative paths to keep trade restrictions in place, keeping policy uncertainty elevated.

Politics aside, markets rebounded broadly on the week. U.S. equities gained more than 1%, led by large caps and growth stocks in a temporary reversal of the early-2026 trend that had favored value and small caps. International equities also posted gains and remain competitive with U.S. markets over longer time frames. Bonds slipped modestly as Treasury yields moved higher.

Q4 GDP surprised to the downside at 1.4%, well below prior estimates that had ranged from roughly 2.5% to as high as 5% in earlier projections. The weakness was largely driven by a sharp decline in government spending. Under the surface, consumer spending grew at a solid 2.4% pace and business investment rose 3.7%, suggesting the private sector remains on firm footing.

This Week

It is NVIDIA week. The company reports after market close on Wednesday, and with a weighting of more than 7% in the S&P 500, its results and guidance carry outsized influence. Given its central role in the AI buildout, the report has the potential to move not only semiconductor stocks but broader market sentiment.

The economic calendar is lighter following last week’s wave of data. Producer Price Index data will be the primary release, offering another read on inflation trends after December’s hotter-than-expected PCE print.

Policy expectations remain steady. Markets are pricing a 97% probability of a hold at the March 18 Fed meeting. Meanwhile, the Atlanta Fed GDPNow model has begun tracking Q1 growth at 3.1%, offering an early look at how momentum may be evolving after the softer Q4 print.

We hope you have a great week. If there’s anything we can do to help you, please feel free to reach out to ben.vaske@orion.com or opsresearch@orion.com.