Our investment team is closely monitoring the developments in the Middle East and the impact they are having on commodity prices, the stock market, and the world economy. We lament the loss of innocent life, pray for the safety of U.S. troops in harm’s way and mourn the U.S. military servicemembers who have lost their lives.

You will continue to hear from us on the conflict with Iran. In the meantime, if you have any questions on the markets and the economy or if there is anything we can do to support you and your clients during this difficult time, please reach out to us via our Investment Strategy Team’s email address at opsresearch@orion.com.

Weekly Notes from Tim

By Tim Holland, CFA, Chief Investment Officer

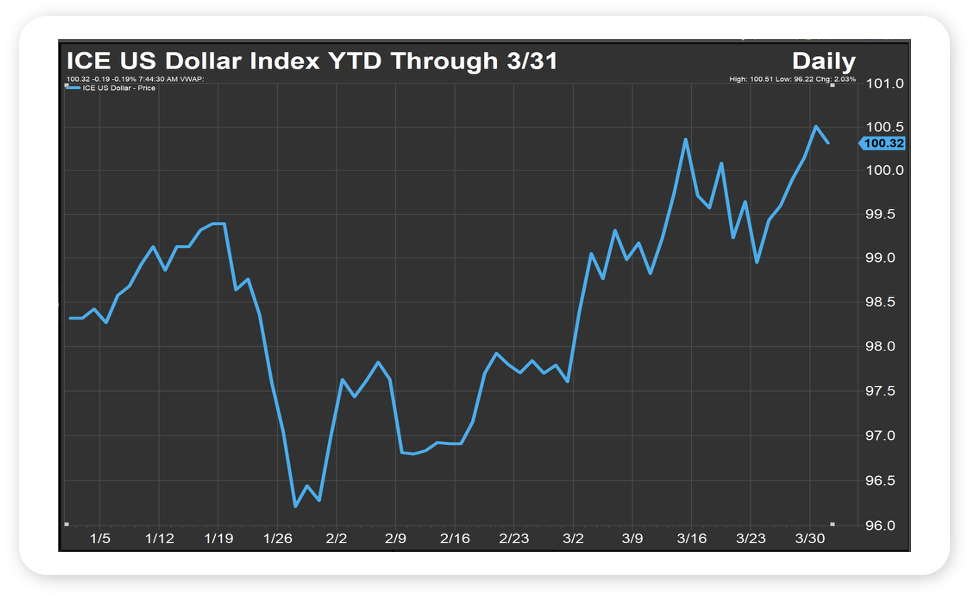

- One candidate for the consensus trade of 2025 was shorting the dollar. As to why traders were bearish on the world’s reserve currency, reasons included large US fiscal deficits; foreign central banks buying more gold (and fewer dollars); less than friendly nations building out non-dollar based trading regimes and nations of all stripes moving away from the dollar specifically – and US financial assets generally – as they believed the US was becoming a less reliable partner, a conclusion driven by disagreements over trade and security policy. And that bet paid off handsomely last year, with the Greenback falling 10% (per the ICE US Dollar Index).

- While one can make the case that the headwinds cited above remain and the dollar is destined to fall further, it has rallied in 2026, with the ICE US Dollar Index up about 2% year to date and up about 5% from the 13 year low it hit on January 27th (as of 3/31/26; see chart). As to why the dollar has caught a bid of late, pundits might point to a global flight to safety (US financial assets, including the dollar, tend to be bought during periods of geo-political risk); a Federal Reserve that could be done cutting rates, and poised to raise them; foreign central banks buying less gold as their nations spend more on oil, and a US economy likely to outperform through a period of elevated energy prices (the US leads the world in crude oil and natural gas production and is a net exporter of energy products).

- Currency markets are notoriously difficult to forecast near-term, so we won’t make a call on how the dollar might trade over the coming days and weeks. That written, the US economy remains the world’s largest, and arguably its most diverse and innovative; the US is home to the world’s largest, most liquid stock and bond markets and the US is the world’s preeminent military power. One bet we are comfortable making is the dollar isn’t losing its reserve status anytime soon.

Source, Factset March 2026

Looking Back, Looking Ahead

By Ben Vaske, BFA, Manager, Investment Strategy

Last Week

Markets saw a strong rebound last week, marking the best week of 2026 so far, though sentiment remained heavily influenced by ongoing geopolitical developments. Equities rallied early in the week on optimism surrounding a potential shift in U.S. policy toward Iran, but some of that enthusiasm faded after messaging later in the week suggested the conflict may persist longer than hoped.

Economic data pointed to continued resilience in the U.S. economy. Nonfarm payrolls came in well above expectations with 178,000 jobs added and the unemployment rate declined to 4.3%, reinforcing the strength of the labor market. Other data was generally stable, with retail sales meeting expectations, manufacturing remaining in expansion territory, and the trade deficit coming in better than expected.

Performance reflected improving sentiment overall. U.S. equities posted broad-based gains across sizes and styles, while international markets also moved higher. Small caps returned to positive territory for the year, though large caps still lag year to date. Interest rates declined despite elevated oil prices, providing support to fixed income, with core bonds gaining nearly 1% on the week. Commodities continued their strong run as oil prices remained elevated.

This Week

Geopolitics will remain front and center as the U.S. continues to push toward a resolution with Iran. Markets will be closely watching for updates, including a potential national address, as any signal of escalation or de-escalation is likely to drive short-term market direction.

It is also a heavy week for economic data, with inflation taking center stage. Both CPI and PCE will be released, along with another revision to fourth quarter GDP. With oil prices remaining elevated, investors will be focused on whether inflation continues to trend higher and how that may impact the Federal Reserve’s policy outlook.

We hope you have a great week. If there’s anything we can do to help you, please feel free to reach out to ben.vaske@orion.com or opsresearch@orion.com.