If you’ve opened any financial publication in the last several months, you’ve likely seen numerous headlines in some iteration of “Private Credit Fund Limits Redemptions, Share Price Falls.” To most investors, the sensationalism of news headlines can exacerbate expectations over how these private lenders operate, why they may choose to limit redemptions, and how large of an impact any private credit “meltdown” may truly have on the US stock market and economy. As you have also likely seen, there is a push from the US government to “democratize” access to private or alternative investments, which have historically been exclusive to accredited investors, further increasing the spotlight on these firms and their products.

I’ve recently spent time with two members of Orion’s Private Investments Committee, Will Girton, CFA, and Ryan Karch, CFA, who co-authored today’s piece. There are several goals we had when structuring today’s note, but overall, we’d like to provide context on what we’re seeing in the private asset space and provide reasonable expectations for what may be on the horizon.

Decoding the Private Credit Fund Structure

Private credit as we know it today truly emerged in the 1980s as smaller or riskier companies needed alternative sources of debt financing. Alongside this new source of financing came an amendment to the Investment Company Act of 1940 or “’40 Act” establishing the fund structure we know as a Business Development Company (BDC). A few highlights from this regulation which laid the groundwork for how BDC’s generally operate include:

- Invest primarily in private or small public companies

- Allocate at least 70% of their assets in small, developing, or financially distressed companies

- If a BDC distributes 90% of its taxable income to shareholders, it is exempt from corporate taxation

- Operate with more flexibility around leverage than traditional ’40 Act funds, typically capped at 2:1 leverage

BDC’s attract investors by offering 1) higher risk premiums – portfolio companies tend to be smaller, riskier, or distressed, meaning they must generate higher returns to attract investment and 2) an illiquidity premium – invested assets generally have lockup periods and limited redemption levels due to the long-term nature of the underlying loans.

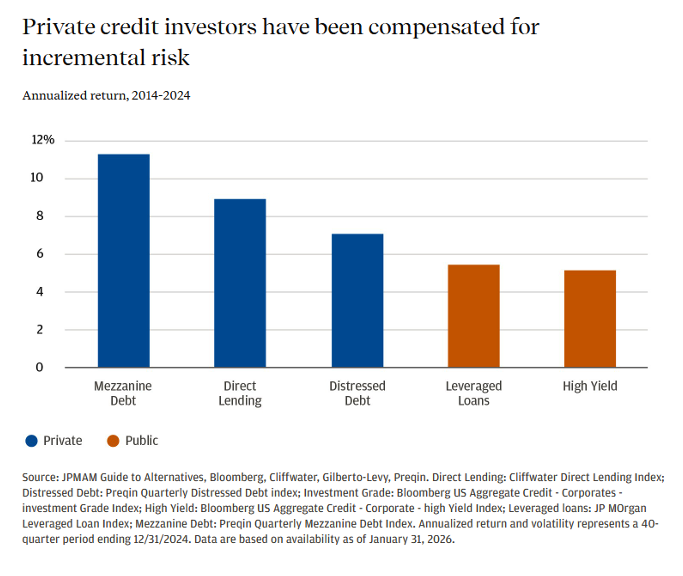

According to JPMorgan’s Guide to Alternatives, private credit investors have historically been compensated, as expected, with these elevated risk and liquidity premiums. Over the 10-year period from 2014-2024, direct lending has achieved a roughly 4% annual spread over publicly traded high yield debt.

At the risk of over-explaining, there are a few more BDC-specific terms we’d like to define before moving on to our thoughts on today’s environment.

- Gating: A temporary limitation on redemptions when withdrawal requests exceed predefined thresholds. This is designed to prevent forced selling and protect long-term investors.

- Repayment hierarchy: In any loan or investment, there is a defined hierarchy for who gets paid back first if a borrower runs into trouble. Senior lenders (like most private credit funds) sit at the top of that hierarchy, meaning they have the strongest claim on a borrower's assets and the greatest likelihood of recovery.

- LBO: A leveraged buyout (LBO) is when a private equity firm acquires a company using a mix of their own capital and significant borrowed money, with the acquired company's assets and cash flows typically serving as collateral for the debt. Private credit investors are generally the source of this borrowed money.

- Payment in Kind (PIK): A flexibility feature where creditors add interest owed to the principal balance of a loan to free up current cash flow for the borrower. While it can boost reported returns, it also increases risk as balances compound over time.

- Covenant: Contractual protections that give lenders early warning signals and influence if borrower conditions deteriorate.

Understanding Today’s Environment

Just this week, reports showed that Blue Owl Capital, one of the industry’s most prominent private credit managers, is facing a 41% redemption request from its Blue Owl Technology Income (OTIC) fund and a 21% redemption request from one of the industry’s largest BDC’s, the $36B Blue Owl Credit Income Corp (OCIC). These levels of redemption requests are nothing to balk at and have an eerily similar feeling to a bank run, but we don’t think the repercussions are poised to be quite so extreme.

Illiquidity is a feature, not a flaw, of private credit funds. When redemption demand spikes, funds can implement gates to avoid selling long-duration, illiquid loans at distressed prices. This is designed to preserve value for remaining investors and maintain portfolio stability. Rapidly fluctuating asset levels can prove challenging for BDC’s to manage, hence the gating feature. Additionally, these BDCs generally have pre-set limitations on redemptions. Under SEC regulation, registered private credit interval funds are required to allow investors to redeem a minimum of 5% of net assets per quarter. Managers have the latitude to offer higher repurchase floors, but in most cases, 5% per quarter is the norm.

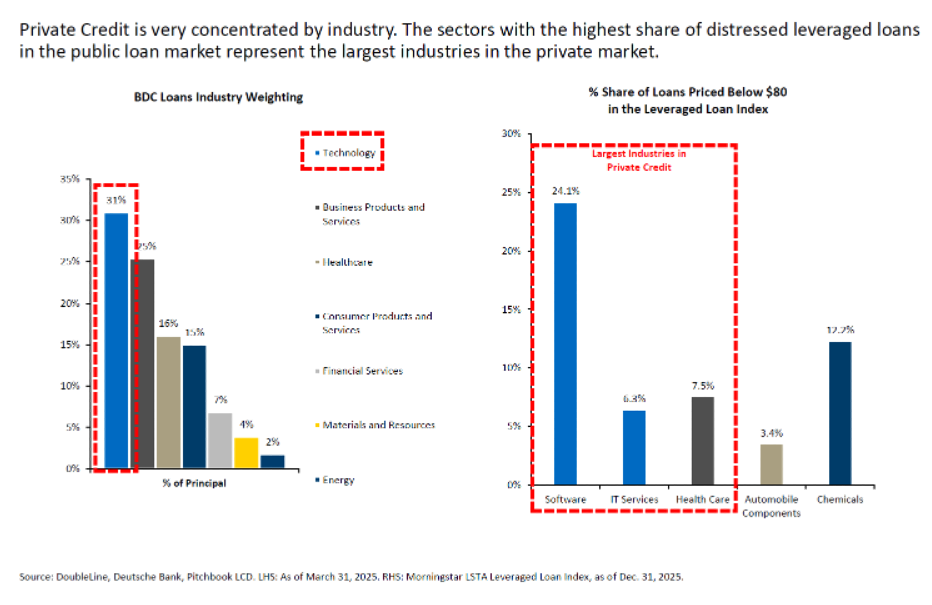

One of the core reasons for today’s stress is not necessarily due to the BDC structure, but rather due to the underlying companies that these BDC’s are invested in. According to research from DoubleLine, there is high concentration in technology and software names within these funds. As publicly traded software companies have been selling off thus far in 2026 with the rapidly evolving AI backdrop, private companies in this sector are exhibiting some stress and leaning more on PIK as their cash flows are constrained as developing companies.

Historical Context

As a point of reference, the private credit market is currently estimated to be about $1.5 – $2.0 trillion. Conversely, the public credit (bond) market is estimated to be roughly $50 trillion in assets, meaning the private credit market is only about 3-5% the size of the public market.

While our hope is of course for private market stress to subside, any kind of wash out is far less likely to lead to mass financial contagion simply due to its relatively small size. Compare this to the Global Financial Crisis where the subprime mortgage market was closer to 15% of the overall mortgage market and default rates reached upward of 25% by 2008.

Fundamentals Under Scrutiny

- Roughly 80-90% of private credit loans are floating rate, with interest payments tied to SOFR (market benchmark rate) plus a spread

- As a result, debt burdens for borrowers become increasingly challenged with higher real rates, something we are monitoring closely

- Persistent energy shocks and inflation likely lead to negative pressure on earnings and margin compression, compromising borrowers’ ability to pay down debt

- It’s estimated that about 65-75% of private credit originated loans in North America are sponsor backed loans – loans to the portfolio companies of private equity sponsors

- Why that matters?

- Private equity sponsors have a vested interest in growing the equity value of their portfolio companies over time

- According to Burgiss, about 80% of private credit loans are senior secured in the capital structure or 1st lien in order of claims. Meaning the equity sponsor will take first losses (up to their equity commitment) before the credit is impaired

- Importantly, as highlighted in the Doubleline table above, it is believed that software deals account for roughly ¼ of all sponsor-backed LBOs since 2020, due to what were considered strong recurring revenues and predictable cash flows along with asset light balance sheets. In our opinion, this is where the real stress lies as those assumptions are increasingly challenged.

- Why that matters?

- Default rates remain low at 1-2%, though alternative financing structures like PIK may mask underlying stress and underestimate true defaults

What Matters From Here

In this environment, manager selection and diligently questioning client suitability are critical steps. Exposure to sectors like software varies widely across private credit portfolios. So does underwriting discipline, covenant quality, and the willingness to lean on PIK structures. Private credit, simply put, is not an asset class where all exposures are created equal, and suitability still varies by investor, despite efforts to democratize access to these investments.

For advisors, the focus should remain on:

- Understanding the underlying portfolio exposures and how they fit within a portfolio

- Evaluating how managers are navigating borrower stress

- Reinforcing the role of time horizon and illiquidity with clients

Private credit was never designed to provide daily liquidity or short-term optionality. It was designed to harvest a premium over time in exchange for reduced liquidity. With larger asset bases, reserving a portion of investable assets for illiquid investments that may require a time horizon of 5+ years can be a prudent choice to capture the aforementioned benefits of private investments. However, smaller client accounts, highly risk averse clients, or clients with nearer term liquidity needs are likely not strong targets for private credit investments.

In Conclusion

In our opinion, private credit is neither risk-free nor fundamentally broken. What we are seeing today is a combination of structural features working as intended and pockets of fundamental stress emerging in specific areas of the market. At the end of the day, these are credit instruments that are fundamentally exposed to the same credit cycles that underpin the economy. Gating is not inherently a signal of failure, rather, it is a mechanism designed to protect investors in precisely these types of environments. The real risks lie beneath the surface, in borrower fundamentals, sector concentration, and manager decisions.

For advisors and investors, the takeaway is not to react to headlines, but to understand the structure, evaluate the fundamentals, and stay anchored to the long-term role private credit plays within a diversified portfolio.