Our investment team is closely monitoring the developments in the Middle East and the impact they are having on commodity prices, the stock market, and the world economy. We lament the loss of innocent life, pray for the safety of U.S. troops in harm’s way and mourn the U.S. military servicemembers who have lost their lives.

You will continue to hear from us on the conflict with Iran. In the meantime, if you have any questions on the markets and the economy or if there is anything we can do to support you and your clients during this difficult time, please reach out to us via our Investment Strategy Team’s email address at opsresearch@orion.com.

Weekly Notes from Tim

By Tim Holland, CFA, Chief Investment Officer

- Great maxims are universal. An example is Wayne Gretzky’s “Skate to where the puck is going, not where it has been,” which works in hockey but also across any athletic or entrepreneurial endeavor – we should want to be anticipatory, proactive and forward-looking in all that we do. I would argue the maxim also works for markets, that equity prices will skate to where the puck (in this case the economy, earnings, interest rates and geo-political risk) is going. Said differently, markets can and will reflect where fundamentals will be in the future, not where they are today.

- Which is one way, in the face of an ongoing war in the Middle East, elevated oil prices and inflation expectations and depressed consumer sentiment, to explain rallies of 12%+ in the S&P 500, Nasdaq Composite and Russell 2000 over the past few weeks. If one wanted to square the dramatic rebound in risk assets with still concerning economic and geo-political backdrops, one could make the following argument…

- The spike in the price oil and any impact it will have on inflation will prove transitory

- Q1 earnings season will see the S&P 500 deliver its sixth consecutive quarter of double-digit earnings growth

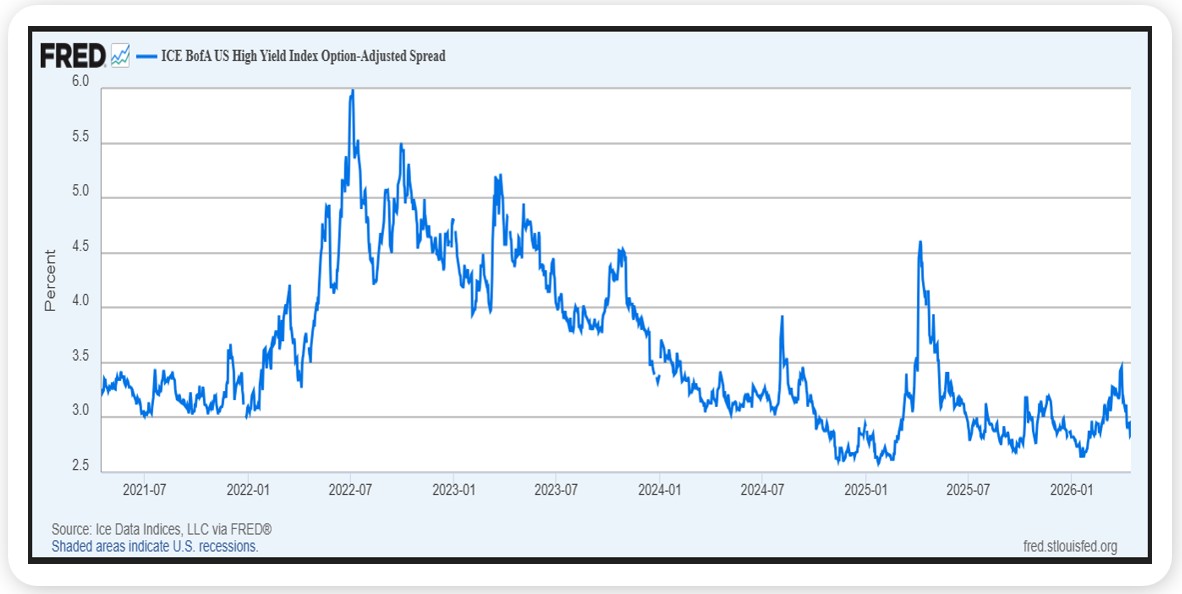

- Concerns over private credit are overdone (high yield bond spreads falling below their late February level are a supporting datapoint; see chart)

- Consumer sentiment doesn’t reflect consumer behavior (big bank CEOs called out a resilient US consumer on recent Q1 earnings calls)

- The AI build out is ongoing and AI won’t meaningfully disrupt software as a service businesses (the Russell 3000 Growth Index is up 17% since March 30th)

- The war with Iran will end soon and, in a manner, more supportive of global growth and geo-politics than most anticipate (for me, this means the Strait of Hormuz is no longer under Iranian control, or at least not fully under Iranian control)

- Of course, the bounce in the market might not prove lasting and our optimistic checklist might not come to pass. That said, I appreciate the fact that the market is a heck of a lot smarter than I will ever be, and for now the market is signaling – I think – better days ahead.

Source, Federal Reserve Bank of St. Louis April 2026

Looking Back, Looking Ahead

By Ben Vaske, BFA, Manager, Investment Strategy

Last Week

Markets extended their strong momentum last week, with U.S. equities rallying to new all-time highs and marking a third consecutive week of gains. The NASDAQ 100 led the move higher, surging over 6% as risk appetite improved alongside a temporary easing in geopolitical tensions tied to the Middle East.

At the same time, oil prices provided some relief, falling more than 10% on the week to close near $83 per barrel. While this helped ease near-term inflation concerns, the situation remains fluid as conflict around the Strait of Hormuz continues, including renewed military activity over the weekend.

Performance was broadly strong across asset classes. U.S. equities posted significant gains, with the S&P 500 up over 12% and the NASDAQ 100 up more than 16% since the recent rally began on 3/31. International equities also benefited from a weaker U.S. dollar, contributing to a global equity market that is now up roughly 7% year to date and still led by non-U.S. markets. Commodities pulled back alongside oil but remain the top-performing asset class in 2026, while REITs have begun to gain traction as rates declined. Interest rates moved lower on the week, with the 10Y Treasury yield falling and mortgage rates declining as well.

This Week

Geopolitics remain a key factor for markets, with U.S. officials set to continue peace negotiations in Pakistan this week. While markets have begun to price in a potential near-term resolution, uncertainty remains elevated and any developments could quickly shift sentiment.

Focus will also turn to the U.S. consumer and corporate fundamentals. Retail sales data this week will provide another read on consumer strength, while a busy earnings calendar featuring major airlines, Tesla, and United Healthcare will offer further insight into how companies are navigating the current environment. Even with lighter economic data overall, these releases will help determine whether the recent market rally is supported by underlying fundamentals.

We hope you have a great week. If there’s anything we can do to help you, please feel free to reach out to ben.vaske@orion.com or opsresearch@orion.com.