Key takeaways:

- Kevin Warsh, who is expected to replace Jerome Powell as the new Federal Reserve chair, has vowed independence from the White House.

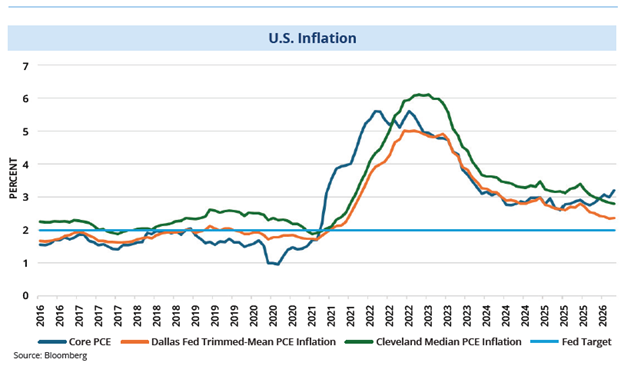

- Under Warsh’s preferred framework, inflation today looks closer to target, giving him cover for rate cuts. Warsh prefers ranges to point estimates, a shift that would widen the goalposts on what constitutes “on target.”

- While his preferred inflation readings may be currently lower than the Fed’s historically preferred reading, they’ve run higher in the past. If that pattern repeats, Warsh would be stuck defending a framework that works against his dovish impulses.

- There is a larger force that may be at work in the Warsh era: AI may be replacing the Fed as the center of gravity for the markets.

Jerome Powell’s final act as Federal Reserve chair played out with a fitting degree of drama: An 8-4 vote at the April FOMC meeting to hold rates steady, four dissents for the first time since 1992 and a departing chairman still waiting for a DOJ investigation to fully close before stepping aside. It was a complicated ending to a tenure that will be debated for years. But the more important question for investors is what lies ahead as a new leader takes the helm.

Kevin Warsh, who cleared the Senate Banking Committee on a party-line vote, is now expected to receive full confirmation before Powell’s term as chair officially expires. He brings five years on the Board of Governors spanning the financial crisis and a well-documented set of views on how the Fed lost its way. Unlike many nominees who arrive with lower profiles, Warsh has been publicly writing and speaking about monetary policy for over a decade. That familiarity is both reassuring and unsettling because his vision of the Fed looks meaningfully different from the one Powell ran.

Don’t assume a dovish pivot

The market’s initial concern was straightforward: Is Warsh just a vessel for the White House’s demands for rate cuts? His Senate testimony pushed back on that notion. He told the committee that the president never asked him to commit to rate cuts and that he would not have agreed to such a condition.

But the rate picture is more nuanced than a simple dove-or-hawk framing. Warsh believes the Fed’s inflation models are broken and that the institution is still dealing with the consequences of the 2021-2022 policy errors. However, the ultimate decision on the federal funds rate policy is not his alone.

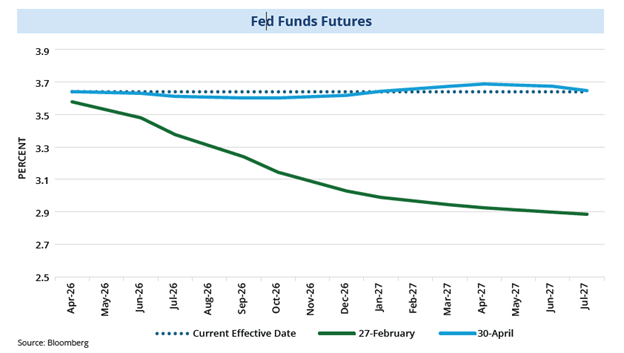

The April FOMC’s four dissents were a message that others may not share his perspective (three of the dissents objected to the FOMC statement’s residual easing bias). Energy prices remain elevated from the Iran conflict, consumer spending continues to hold up and the fed funds futures market is signaling no rate cuts on the horizon. Warsh may want lower rates eventually, but the committee he inherits is not inclined to follow their new leader, at least for now.