After a volatile first quarter, equity markets have shown welcome resilience, with returns improving meaningfully through April and into May. This recent strength reflects a combination of better-than-expected economic data, continued earnings growth, and a U.S. consumer that, despite elevated price levels, remains in relatively healthy shape.

At the same time, however, markets are increasingly grappling with a familiar concern: inflation. While price pressures moderated from their 2022 peaks, they have not fully returned to the Federal Reserve’s 2% target and, more importantly, may be showing signs of reacceleration.

What is the Backdrop for Equity Markets?

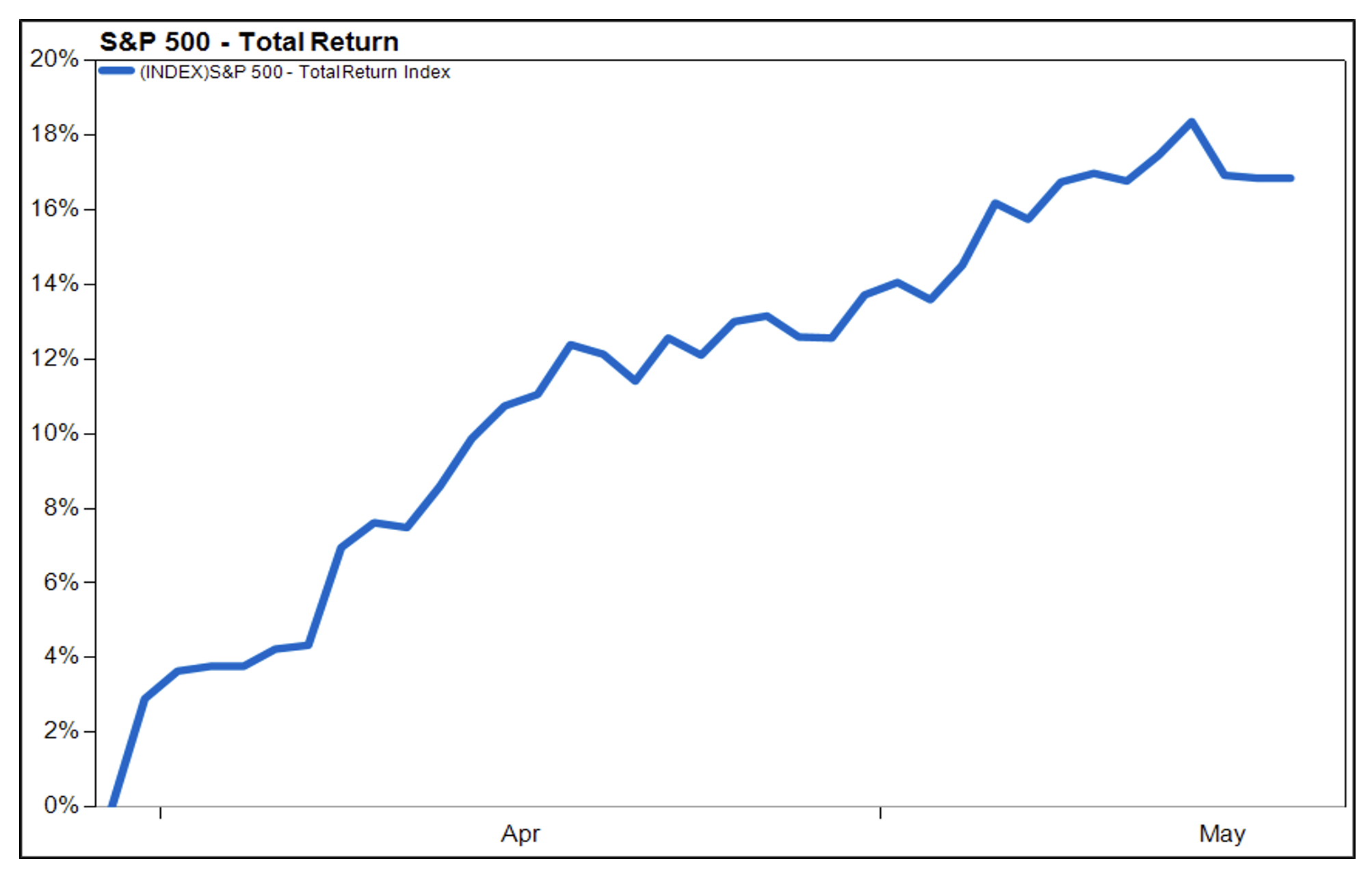

The backdrop for equities is quite positive. Stock prices have responded positively to de-escalation developments in Iran and another stellar quarter of corporate earnings growth. Since near-term lows on March 30th, the S&P 500 has rallied higher by approximately 17% while the NASDAQ advanced 26%.

Source: FactSet, May 2026

That said, the macro environment is far from benign.

Inflation remains above target, with recent data renewing upward pressure. Energy markets are unbalanced, particularly following geopolitical tensions in the Middle East; and the Federal Reserve is in a tough spot, balancing a cooling labor market against persistent inflation risks.

This combination has kept monetary policy expectations in flux. While investors had been anticipating rate cuts earlier in the year, inflation’s “stickiness” has pushed markets toward a more cautious stance reflected in higher yields across the yield curve. Investors are now pricing in zero rate cuts for 2026, with odds of a rate hike also increasing.

A Message from the Bond Market

Perhaps the most important development beneath the surface is the bond market’s response. The 10-year U.S. Treasury yield has moved above 4.60%, a level last seen in 2023. In simple terms, the bond market is increasingly pricing in the likelihood of future inflation. Rising long-dated yields serves as a reminder that investors cannot simply ignore ongoing price pressures.

In this context, the bond market is effectively pushing back against the view that inflation is “solved,” reinforcing the idea that monetary policy may need to remain restrictive for longer.

As we saw in 2022, higher bond yields have the power to move the needle closer to a risk-off environment, particularly for segments of the market that are more sensitive to borrowing costs, including smaller companies and growth stocks.

A Leadership Change at the Fed Adds Another Layer

One of the key questions facing markets is whether we are experiencing a temporary inflation bump—or something more structural?

It is undeniable that the post-COVID environment represents a sustained shift relative to the low-inflation backdrop of the 2010s.

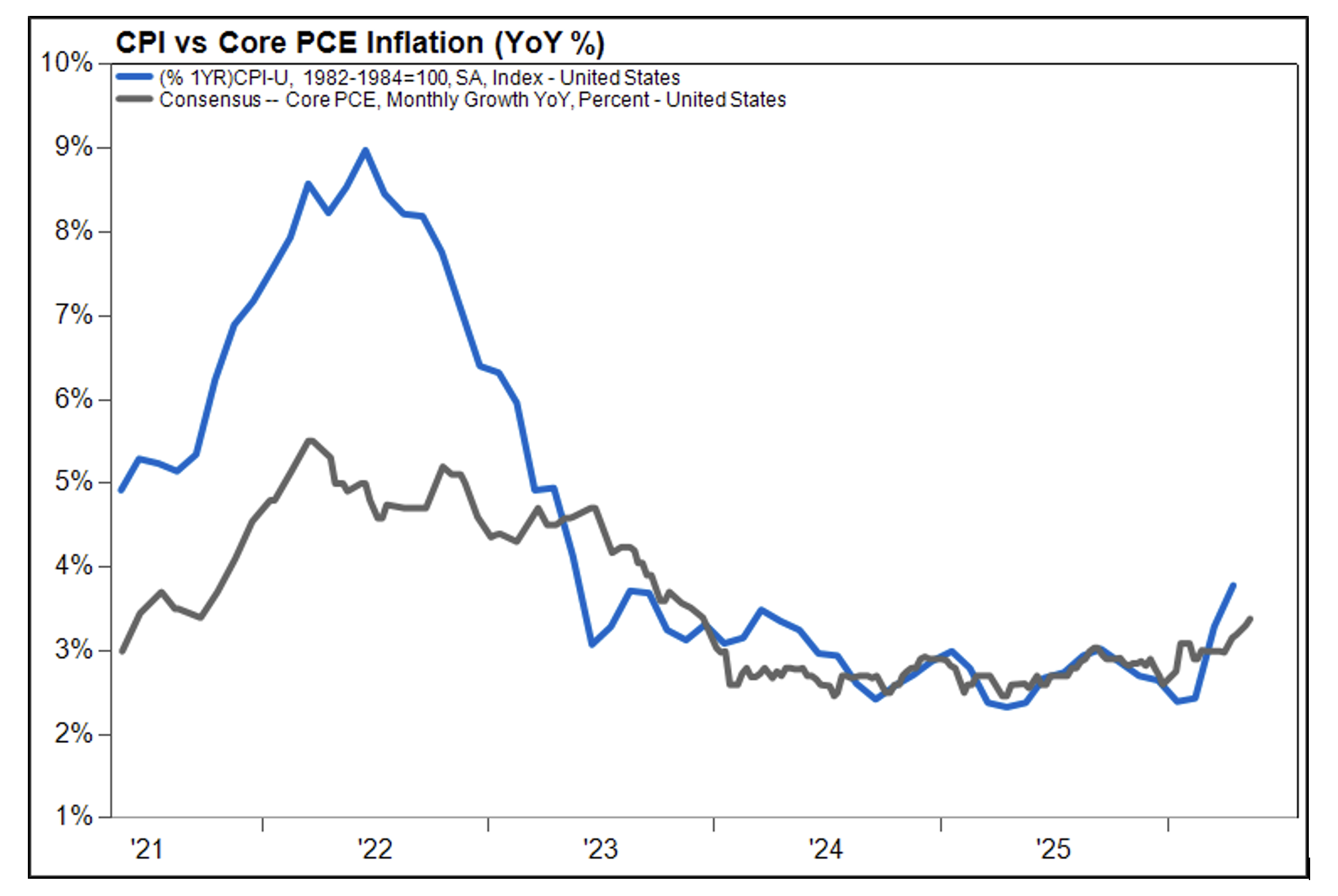

Supply-side factors, including energy and global trade dynamics, are running particularly hot. The Core Personal Consumption Expenditures (PCE) Index rose to 3.2% in March, with the pace expected to accelerate in the coming months. Headline inflation, or CPI, jumped to 3.8%, its highest reading since 2023.

Source: FactSet, May 2026

These developments have prompted increased comparisons to past cycles - particularly the 1970s - where energy shocks and policy missteps led to a second wave of inflation. Price pressures during that period were driven by a combination of loose monetary and fiscal policy, an environment that was amplified by structural and institutional shifts, including a pivot away from the gold standard (pegging currency supply to gold reserves backed by governments), which made inflation more persistent and self-reinforcing. Geopolitical events in the Middle East also represented familiar catalysts, as oil crises in 1973 (oil embargo against the US, by Arab states) and 1979 (Iranian revolution) added unprecedented volatility.

While there are important differences today (including stronger U.S. energy independence and a service-based economy), the parallels are enough to keep investors on edge.

Compounding the uncertainty is the transition at the Federal Reserve. New Chair Kevin Warsh has stated publicly that the central bank may lean on “smoothed” datasets going forward. One inflation-specific example is a preference for using the “Trimmed Mean PCE” produced by the Dallas Fed, in contrast to the Core PCE preferred by departing Chair Jerome Powell. The Trimmed Mean PCE removes the most extreme price increases and decreases (outliers) across all spending categories each month. He enters at a time with a divided FOMC, highlighted by three voting members who dissented the dovish language used in the post-April meeting statement, favoring the removal of an easing bias.

Balancing Risk with Opportunity

The geopolitical backdrop, particularly energy-related risks, presents valid uncertainty.

Despite these concerns, the broader macro picture remains constructive. Corporate earnings growth continues to outperform expectations, the U.S. consumer remains resilient, and recent economic data has come in better than feared, reducing the probability of a recession.

Equity markets and investors appear willing to look past macroeconomic concerns, at least for now. While inflation and rising yields are legitimate concerns and deserve close monitoring, the long-term, underlying fundamentals remain supportive of current equity prices.

For financial advisors, the current environment calls for a balanced perspective:

- Respect the signals from the bond market and inflation data.

- Acknowledge that policy may remain tighter for longer.

- But also recognize the durability of earnings, the consumer, and the broader economy.

Orion’s investment team continues to advocate for diversified portfolios, which served investors well in the first quarter. Taken together, our outlook remains cautiously optimistic, with the potential for higher equity returns and another leg of the bull market still in play.