Our investment team is closely monitoring the developments in the Middle East and the impact they are having on commodity prices, the stock market, and the world economy. We lament the loss of innocent life, pray for the safety of U.S. troops in harm’s way and mourn the U.S. military servicemembers who have lost their lives.

You will continue to hear from us on the conflict with Iran. In the meantime, if you have any questions on the markets and the economy or if there is anything we can do to support you and your clients during this difficult time, please reach out to us via our Investment Strategy Team’s email address at opsresearch@orion.com.

Weekly Notes from Tim

By Tim Holland, CFA, Chief Investment Officer

- 2026 has been volatile but positive for US equities – as we take pen to paper, the S&P 500, Nasdaq and Russell 2000 are up between 9% and 16% year to date. As to where stock prices head from here, we think that probably comes down to an old school, toe-to-toe slugfest – think Ali / Frazier I, II or III or Hagler / Hearns, which for my money is the greatest fight ever – between the heavyweights of Wall Street: earnings and interest rates (think interest rates and bond yields).

- We believe earnings and interest rates drive equity prices long-term. As it concerns earnings, equity investors want to see earnings growth that is consistent and consistently above expectations. As it concerns interest rates, equity investors want to see interest rates and bond yields moving sideways to down (but not down too quickly or too sharply as that could imply an economy that is at risk of or already in recession). Equity investors also don’t want to see interest rates and bond yields moving too high, too quickly as that could imply an economy that is or will soon be dealing with too much inflation, while also pressuring share prices as bonds become more attractive relative to stocks and future corporate earnings are worth less (equity investors discount back expected earnings to determine what a stock is worth today; a lower discount rate makes those earnings worth more, a higher discount rate makes those earnings worth less).

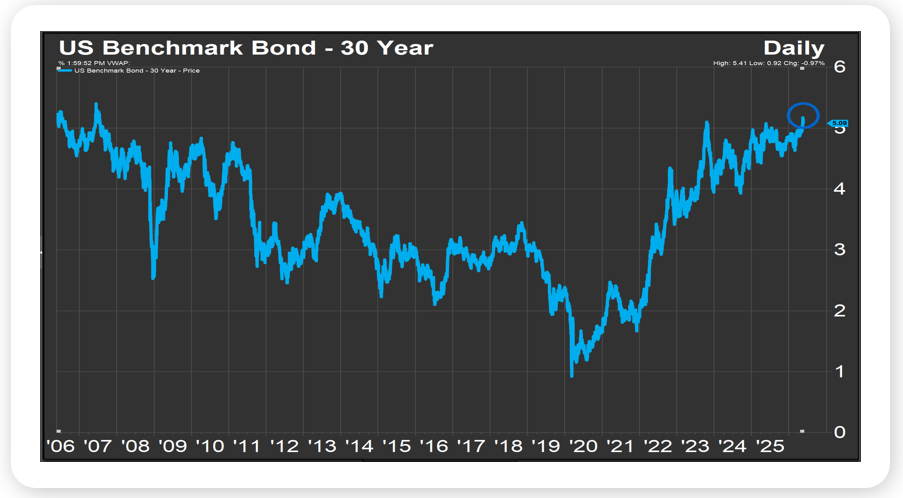

- One could make the case that fight night has arrived, that earnings and interest rates are making their way to ring and that both look pretty darn imposing…consider that S&P 500 Q1 earnings grew 27% year on year while an above average four-fifths of companies topped expectations and that Wall Street expects full year S&P 500 earnings to grow 21%; that said, the yield on the US 30 Year Bond just hit a 19 year high (see chart), the most recent CPI reading came in at 3.8%, higher year on year and hotter than expected, and investors are pricing in a rate hike at the Fed’s December 2026 meeting. So, who might win this hypothetical bout of ours – will 2026 earnings prove powerful enough to overcome higher rates and yields and push stocks higher still, or will higher rates and yields prove too much for earnings to handle, knocking share prices out? My money is on earnings. And my wish is that you all have a happy, safe and fun summer.

Source, FactSet, May 2026

Looking Back, Looking Ahead

By Ben Vaske, BFA, Manager, Investment Strategy

Last Week

Equity markets delivered another solid week, with value stocks and small caps leading broad-based gains and major indexes closing at all-time highs. Fixed income and international equities also posted positive weeks despite interest rates and the U.S. dollar finishing little changed. Taking a look at last-twelve-month returns, diversified portfolios have been exceptional by historical standards, with all major equity classes up at least 22% and non-equity asset classes such as bonds, real assets, and alternatives providing meaningful ballast against volatility and rising prices. Emerging markets, despite their sharper pullback during the early 2026 geopolitics-driven volatility, are having another strong month and remain the leading equity class year-to-date.

The week's most notable headline outside of markets was SpaceX's announcement of its plans to go public in what would be the largest IPO in history. The company was valued at approximately $1.25 trillion following its February merger with Elon Musk's AI startup xAI.

On the economic front, consumer sentiment hit an all-time low, with the University of Michigan reading falling below the troughs seen during the last five recessions. High gas prices, persistent inflation, the ongoing conflict in the Middle East, and a widening K-shaped economy continue to weigh heavily on the consumer outlook, even as asset prices remain elevated.

This Week

Friday brings the two key releases of the week: the second revision to Q1 GDP and the latest PCE inflation reading, which remains the Fed's preferred gauge of inflation. Expectations for the GDP revision hold at roughly 2% growth for Q1, while Q2 growth estimates as tracked by the Atlanta Fed GDPNow have climbed to 4.3%. Markets are pricing a 99% probability of a hold at the June 17th FOMC meeting, making the inflation data more consequential for the longer-term rate outlook than for near-term Fed action. On the earnings calendar, Salesforce and Dell headline a quieter week as we approach the end of what has been a historic earnings season.

We hope you have a great week. If there’s anything we can do to help you, please feel free to reach out to ben.vaske@orion.com or opsresearch@orion.com.