Key Takeaways

- Consumer sentiment hit an all-time low in late May, and investor sentiment has been below average for over a year despite indexes at record highs.

- Sentiment has historically been a contrarian indicator, and periods of above-average fear and pessimism have created opportunities for disciplined investors, as we’ve already seen in 2026.

- The stock market and the economy are different, and investors’ feelings about short-term economic dynamics, geopolitics, and policy should have a limited impact on investment strategy.

- Poor sentiment creates an opportunity for financial advisors, as fear can lead to emotional decision-making. Disciplined and level-headed advisors can earn their fee by keeping their clients on track, regardless of their emotions.

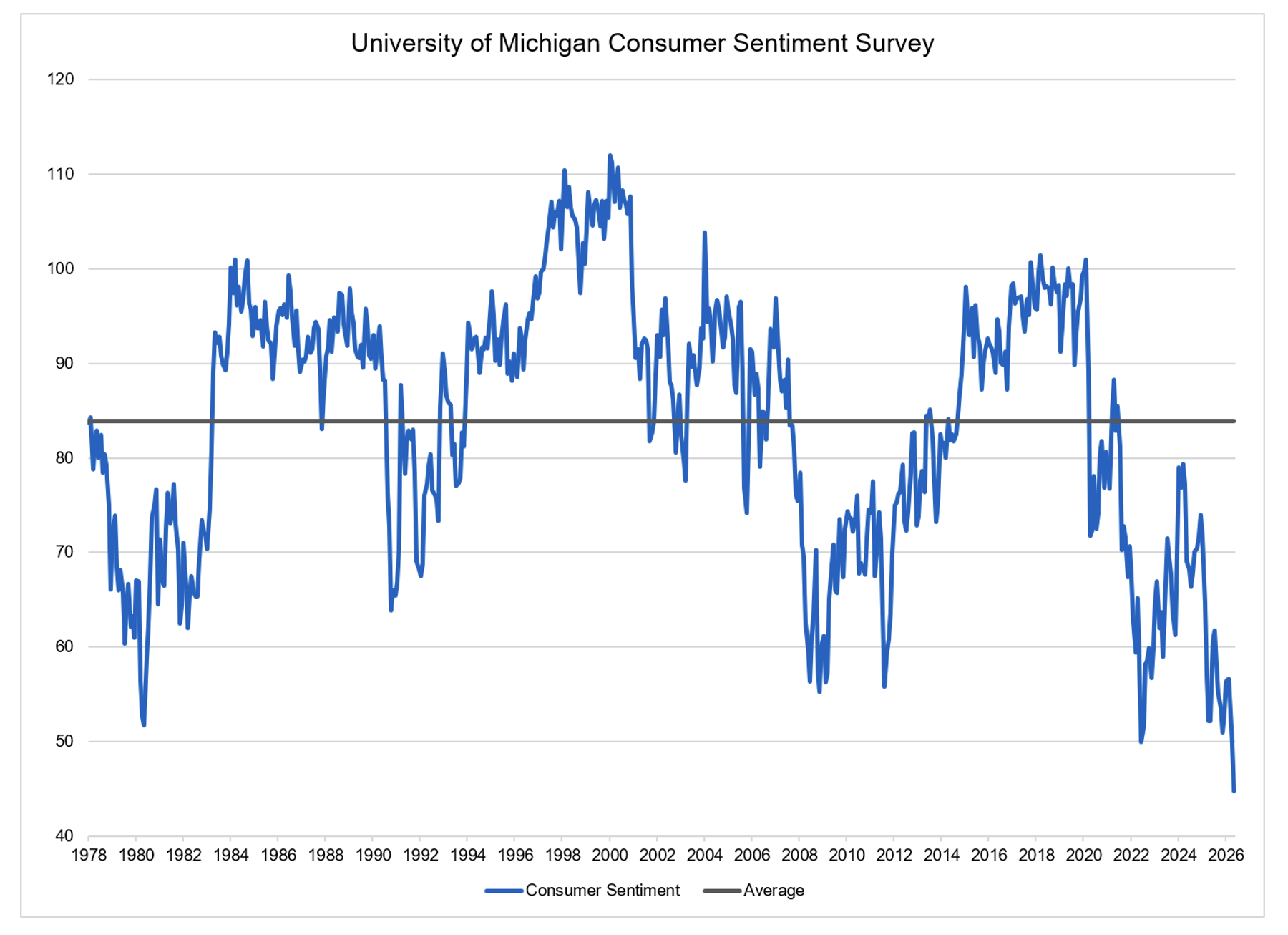

In February 2020, the University of Michigan Consumer Sentiment Survey sat at a rosy 101, in the 93rd percentile of readings since 1978. The index understandably plunged over the next few months during the pandemic, but while financial markets recovered relatively quickly from their initial shock, consumers weren’t so quick to move on. In fact, the consumer sentiment index has only spent six months (out of 75) above its long-term average since March 2020 and recently plunged to its lowest reading ever (44.8):

Source: University of Michigan Surveys of Consumers

As we’d expect, inflation appears to have a predominant effect on consumer sentiment, as this index is driven mostly by economic factors instead of market factors. The two next-lowest readings were in 2022 and 1980, which coincide with the two largest inflationary spikes in this time horizon. CPI inflation has averaged over 4% since 2020, applying consistent pressure on consumers’ wallets and economic opinions. The conflict in Iran and the closure of the Strait of Hormuz have lifted both current and expected inflation, sending sentiment readings plunging to all-time lows.

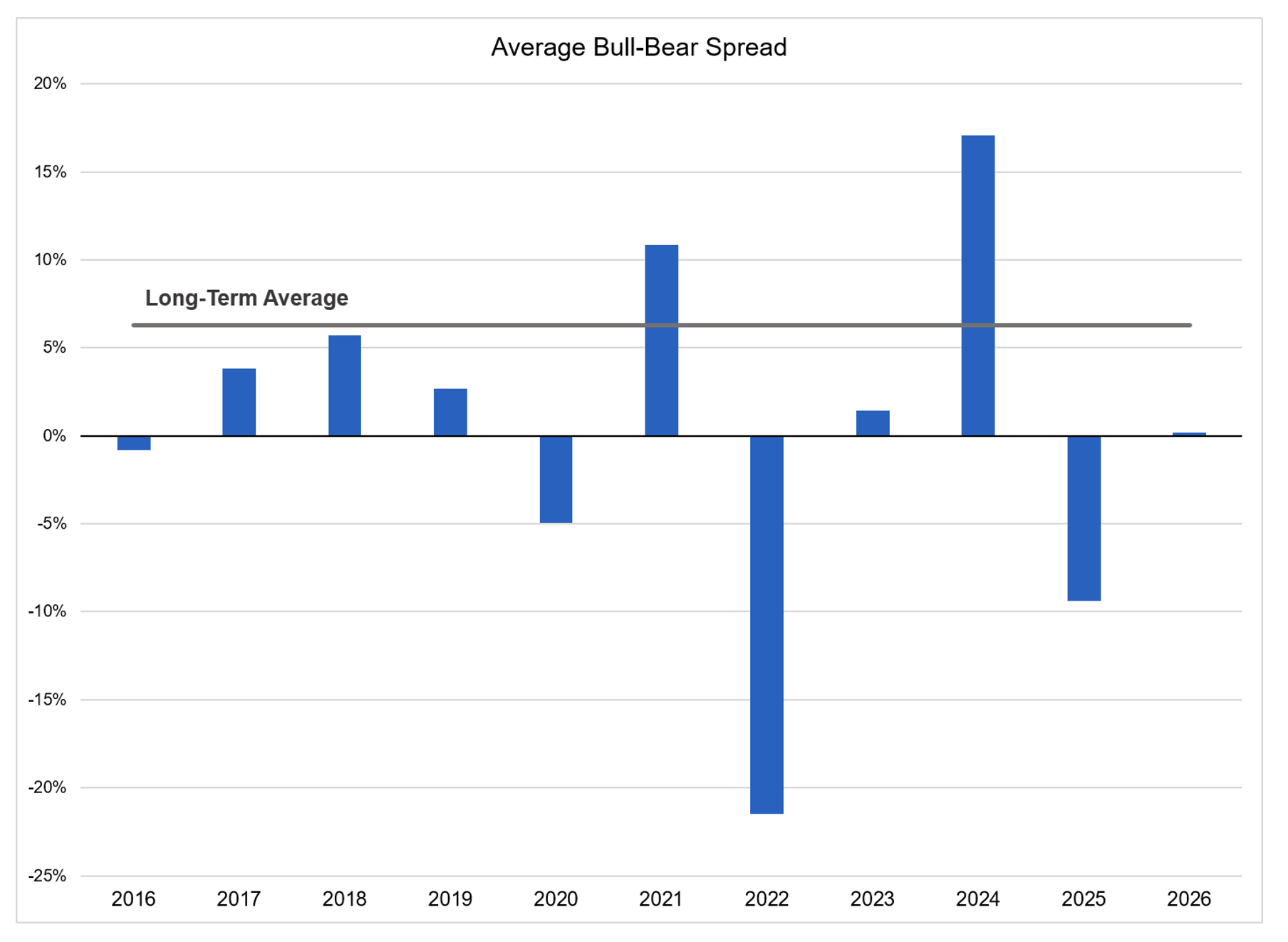

Investors, who have fared far better than consumers in the 2020s, have still struggled to overcome the negativity. While certainly related to consumer sentiment, investor sentiment is driven less by macroeconomics and more by factors driving financial market expectations, including earnings growth and interest rate expectations. After a historically bullish 2024, the AAII Sentiment Survey has reflected above-average bearishness in 2025 and 2026, despite dozens of new all-time highs and an S&P 500 total return of 29% since January 2025. Negative pressures like heightened volatility, stretched valuations, and inflation concerns appear to currently outweigh the positives like robust earnings growth and increasing productivity.

Source: AAII Sentiment Survey

These survey readings paint a difficult picture, which, paired with news programs and social media posts designed to elicit emotion, may have clients nervous or concerned for the future. Below are important points to consider when negativity persists.

1. What investors are saying does not always reflect what they are doing

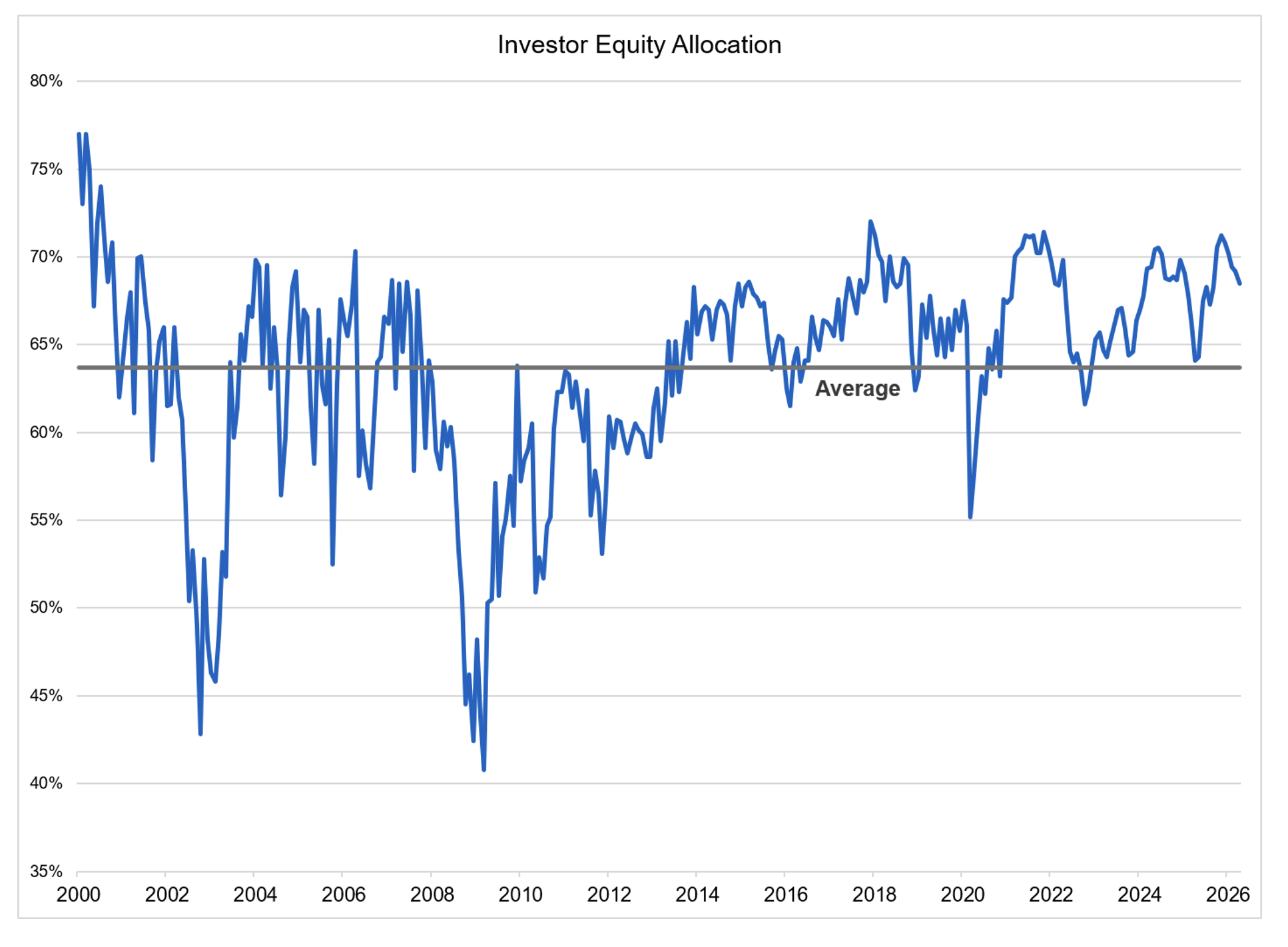

We’ve noticed that historically, bearish sentiment towards equities does not necessarily lead to selling activity. In fact, equity allocations have been rangebound at an above-average level for about a decade, and short-term sentiment shocks have not resulted in significant allocation changes outside of this range. Passive flows, buying-the-dip activity, and the fixed income bear market are all potential contributors to the stability of equity allocations through volatility.

Source: AAII Asset Allocation Survey

2. Sentiment has historically been a contrarian indicator

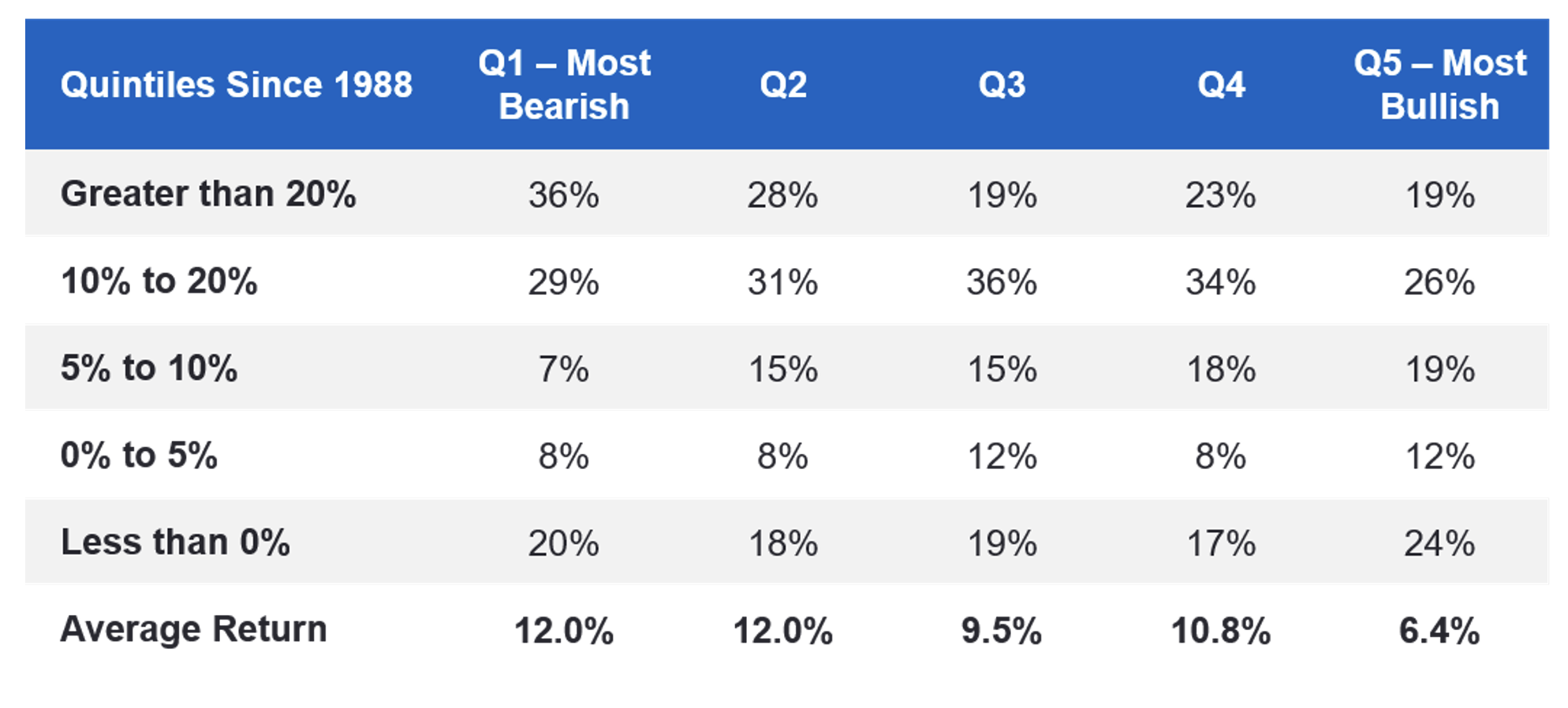

Perhaps one of Warren Buffett’s most well-known quotes is “be fearful when others are greedy, and be greedy when others are fearful.” As is true for most of Mr. Buffett’s investing advice, this has proved profitable throughout history. Sentiment is notoriously a contrarian indicator, meaning its current reading may have an inverse relationship with future returns. Exuberance can lead to crowded trades and overshooting, while extreme pessimism can cause panic selling – both of which are typically remedied by markets in short order once the trading activity is exhausted.

This table from Orion’s Quarterly Reference Guide breaks down every reading from the AAII Investor Sentiment Survey into five quintiles, then shows the probabilities of the forward 12-month return of the stock market at different levels of investor sentiment. Interestingly, the stock market is most likely to produce a negative return over the twelve months following the most bullish investor sentiment, while the most bearish periods have the highest average forward return and the highest probability of 20%+ returns over the next year. The average bull-bear spread in 2026 so far is around 0.1%, falling in the second quintile.

Source: Orion Quarterly Reference Guide, AAII Sentiment Survey

3. Pessimism, fear, and uncertainty create opportunities for financial advisors to promote better investor behavior

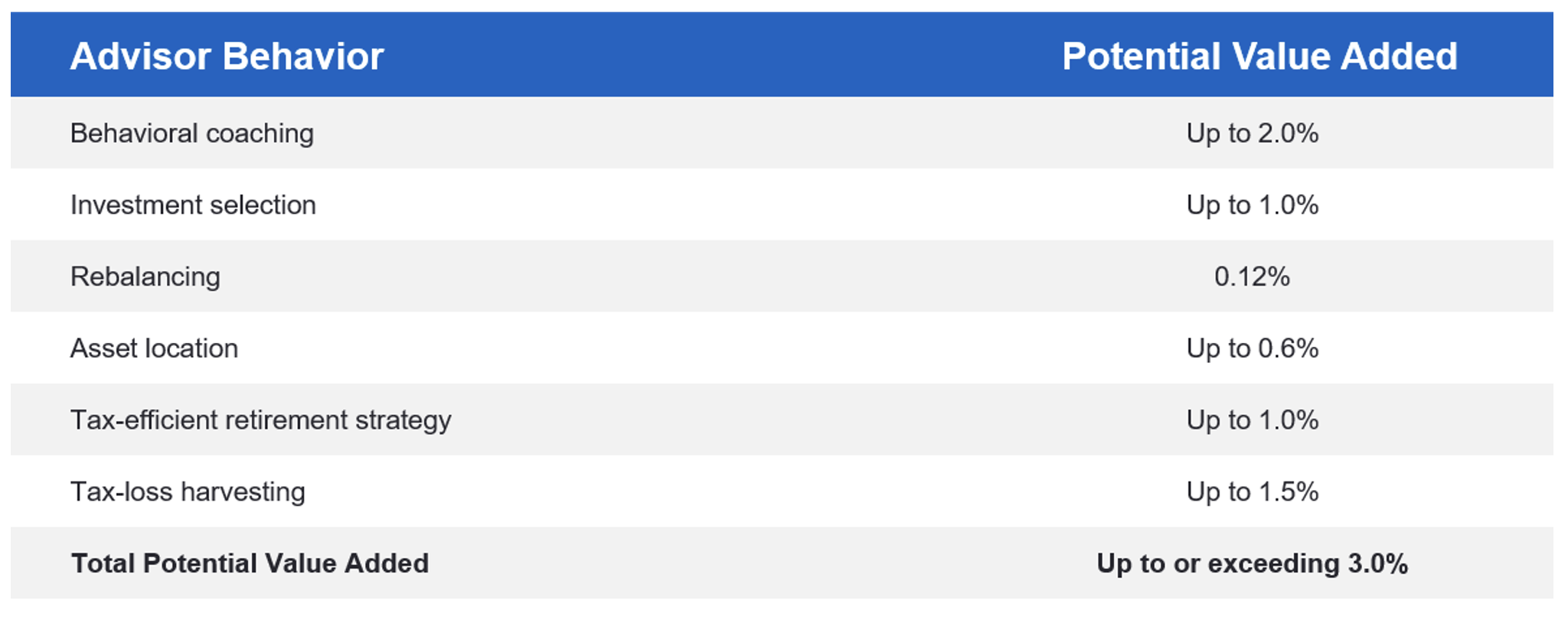

The value of financial advice can be hard to quantify, as relationships are forged over time and throughout market cycles. However, several asset managers have done studies to approximate the potential alpha advisors can provide for their clients, as well as the difference sources of that alpha. This study by Vanguard, Advisor’s Alpha, estimates that advisors can add up to or exceeding 3% per year of performance through their many services – up to 2% of which comes from behavioral coaching.

Source: Orion Quarterly Reference Guide, Vanguard

The Reference Guide compiles several other similar studies, almost all of which come to the same conclusion: while advisors add value for their clients in many ways, perhaps none are more valuable than behavioral coaching.

The largest benefits of behavioral coaching don’t happen when everything is business as usual – it’s easy to stay invested and disciplined in those environments. It’s the extreme moments (exuberance or fear) which cause investors to make emotional decisions that deviate from their long-term plan. Advisors can look at the negative sentiment in the markets today and take the opportunity to make a positive impact on investors’ futures.