Key Takeaways

- The labor market has been in a cooling trend, dating back to 2022.

- We are likely at an inflection point, where the US economy may require fewer jobs in the coming years.

- Potential GDP growth will increasingly lean on gains in worker productivity, in lieu of fewer jobs.

- Markets have applauded the recent boost in productivity, driven by AI, which has been supportive of the multi-year bull market to date.

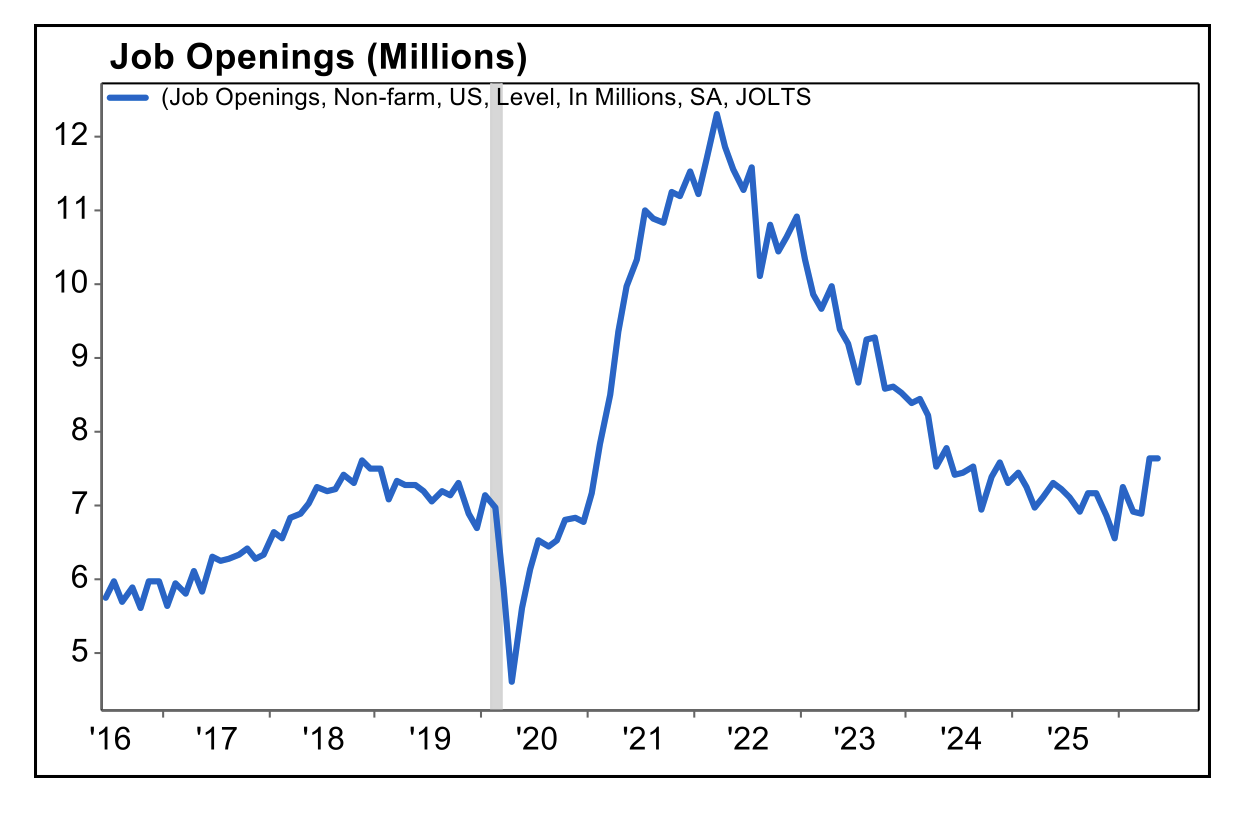

The U.S. labor market is on the precipice of an inflection point after a multi-year cooling process that began in the wake of the post-pandemic hiring surge. The past four years marked a “no hire / no fire” type of corporate environment, as job openings subsided, while the unemployment rate hovered near a healthy 4.3%.

Supply chain disruptions, inflation running much hotter than expected, a spike in borrowing costs, waning immigration growth, and the emergence of artificial intelligence help explain the cooling jobs market to date. These trends raise an interesting question, does the US economy need fewer jobs going forward? For now, we think that answer is “yes.”

Source: FactSet

Grey bar = periods of U.S. recession

What’s Changed in the Labor Market?

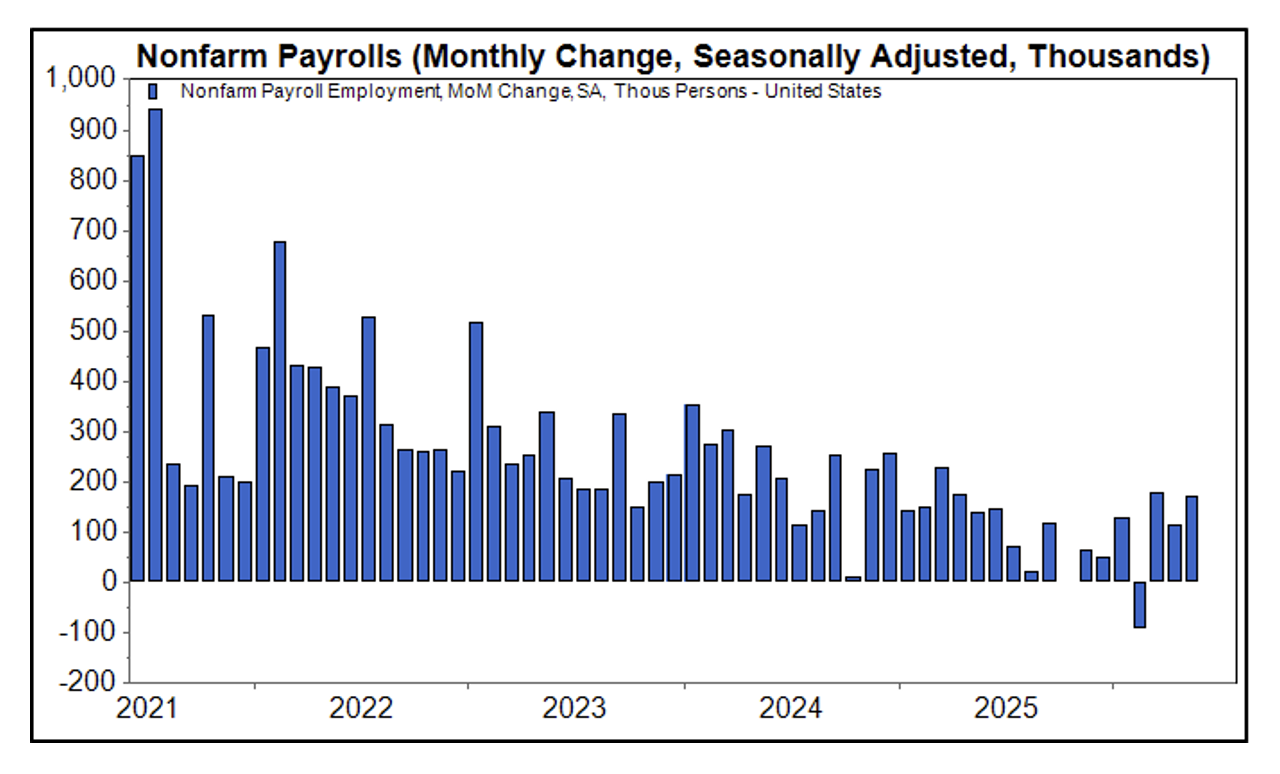

In recent months, jobs data has been surprising to the upside. 172,000 jobs were added in the month of May, which was far better than the 80,000 jobs expected by Wall Street analysts. Payroll gains have averaged 188,000 over the past three months, the highest pace since 2024. Importantly, the unemployment rate held steady as well.

Markets have applauded these solid job gains, bucking the deceleration trend of the past few years. Data surprising to the upside has contributed to the approximate 11% year to date return for the S&P 500. That said, many economists – including those at the Federal Reserve – are forecasting an environment where low, zero, or even negative job growth becomes a new reality.

Source: FactSet

Federal Reserve research indicates that the US labor market has reached a breakeven point – suggesting that we have hit a point in time where the labor force has (or is about to) stop growing; so, any potential economic growth must come from productivity.

The Fed’s April 2nd quote is telling:

“It implies that any growth in potential GDP will need to come entirely from productivity growth. These features would represent a significant shift in U.S. labor market dynamics and the composition of economic growth.”

What Does it Mean for Investors and Financial Advisors?

In practical terms, what would have historically been viewed as weak monthly job growth data, may now be consistent with a balanced labor market, fundamentally altering how investors and policymakers interpret employment data.

This includes the Federal Reserve under new Chair, Kevin Warsh. The Fed’s rate cuts under Jerome Powell in 2024 and 2025 are now fully reflected in the balanced labor market. As I noted last month, the Fed can focus its attention on unsettled inflationary pressures.

For investors and financial advisors, the anticipated shift in labor market dynamics is expected to emphasize worker productivity. In an academic sense, potential GDP grows over time through two mechanisms: either changes in potential employment or growth in the average productivity of each worker. We are increasingly leaning into the latter, which has been supportive of the multi-year bull market to date. Productivity growth is a major reason we remain cautiously optimistic on risk assets as we close out the second quarter.