Our investment team is closely monitoring the developments in the Middle East and the impact they are having on commodity prices, the stock market, and the world economy. We lament the loss of innocent life, pray for the safety of U.S. troops in harm’s way and mourn the U.S. military servicemembers who have lost their lives.

You will continue to hear from us on the conflict with Iran. In the meantime, if you have any questions on the markets and the economy or if there is anything we can do to support you and your clients during this difficult time, please reach out to us via our Investment Strategy Team’s email address at opsresearch@orion.com.

Weekly Notes from Tim

By Tim Holland, CFA, Chief Investment Officer

- There isn’t much I can tell you about last week’s Federal Reserve meeting that you don’t already know…as expected, the Fed left the Fed Funds Rate unchanged at 3.50% to 3.75%...somewhat unexpected, the Fed’s updated Summary of Economic Projections (better known as the Dot Plot) had nine Federal Reserve Open Market Committee – or FOMC – members penciling in one rate hike this year, up from none in March, and one FOMC member penciling in one rate cut this year, down from 12 in March – interestingly, new Fed Chair Kevin Warsh declined to submit any projections for the updated Dot Plot. At a high level, as it concerns its economic and inflation outlook, the Fed lowered its growth expectations and raised its inflation expectations for 2026. Not surprisingly, investors responded to the central bank’s more hawkish posture by selling off stocks and bonds and pricing in a higher probability of a rate hike at the Fed’s July meeting.

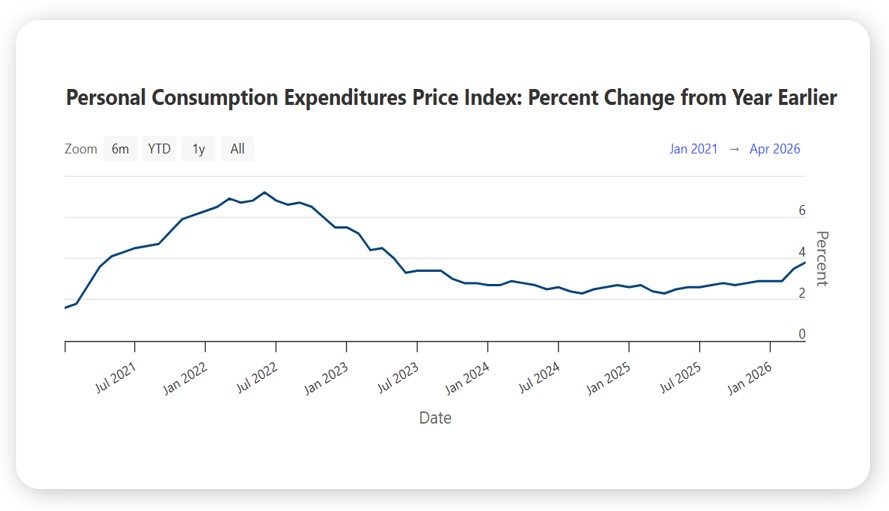

- What might be of some value is calling out what I thought was the most important comment made by Fed Chair Warsh at his inaugural post Fed meeting press conference, and that was “Inflation is a choice.” During his time with the press, Mr. Warsh made it clear the Fed had failed in meeting the price stability half of its dual mandate, noting the Fed’s preferred inflation gauge – the Personal Consumption Expenditures Price Index or PCE – had run ahead of the Fed’s long-term inflation target of 2% for five years (see chart). Mr. Warsh also made it clear the Fed could and would deliver on price stability, which makes sense – if inflation is a choice and not a preordained phenomena, lowering it is also a choice and not beyond the power of the world’s most powerful central bank. If Mr. Warsh needs to establish his inflation fighting bona fides, we think he went a long way towards doing so last week.

For now, investors will probably view the Fed as more foe than friend to risk assets – as we noted recently, a higher cost of capital is almost always unwelcomed on Wall Street – so stocks could struggle near-term. That written, it is worth reminding ourselves of the strong gains US equities have delivered year to date, and of the benefits of an inflation fighting Fed, which should include a stronger US dollar near-term and lower borrowing costs long-term.

Source, US Bureau of Economic Analysis May 2026

Looking Back, Looking Ahead

By Ben Vaske, CFA, Manager, Investment Strategy

Last Week

Global equity markets posted a strong week as news of a potential peace deal between the U.S. and Iran sparked a decisive shift from risk-off to risk-on sentiment. Emerging markets led all asset classes with a gain of nearly 8% on the week, followed by developed international and U.S. tech. Growth stocks outperformed as value lost ground, and oil pulled back to $77 per barrel, now 33% above its pre-conflict level. Interest rates were roughly flat despite the FOMC meeting, leaving fixed income indexes essentially unchanged on the week. The U.S. dollar rebounded approximately 1% to a fresh 52-week high.

Kevin Warsh presided over his first FOMC meeting, where the committee held rates steady but struck a more hawkish tone than markets had anticipated. The updated dot plot was the meeting's defining moment, with nine of eighteen Fed officials now projecting at least one rate hike by year-end 2026, a notable reversal from the two cuts that were being priced into markets at the start of the year. Overseas, the Bank of Japan raised interest rates to their highest level since 1995, a historic pivot for a country that had maintained near-zero or negative rates for decades as it works to combat inflation and support the yen.

This Week

PCE inflation headlines a relatively busy economic calendar, with the reading expected to come in above 4% on Thursday. Flash PMIs, durable goods orders, new home sales, and consumer sentiment round out the week's data slate. The macro backdrop has shifted meaningfully, with markets now pricing a 38% probability of a rate hike at the July 29th FOMC meeting, up from near-zero just a few months ago. On the earnings front, Micron headlines an otherwise light week for earnings releases.

We hope you have a great week. If there’s anything we can do to help you, please feel free to reach out to ben.vaske@orion.com or opsresearch@orion.com.