Key takeaways:

- Investors seem to be making assumptions about who the enduring AI leaders will be, even though history suggests that the AI leaders of today may not be the AI leaders of tomorrow.

- Today’s AI stock valuations demand investors pay for certainties in the AI marketplace that we believe don’t yet exist.

- It could be a while until the AI market’s supply and demand dynamics are settled enough to allow for stable profitability. Past technological shifts signal that it’s unclear at this stage whether current leaders or not-yet-known ones will own most of the profits.

- Current valuations of some of the largest AI firms appear not to fully account for the R&D costs needed for ongoing innovation much less the costs to provide services using current AI models.

AI has the potential to remake our way of life, making it nothing short of revolutionary. It’s no wonder that it has stimulated investor imagination. Wall Street has made spectacular AI growth assumptions – and with high conviction – long before the economics are fully understood. History suggests that the ultimate beneficiaries in the AI ecosystem are far from certain even as investors are betting on who the enduring leaders will be.

To Boldly Go

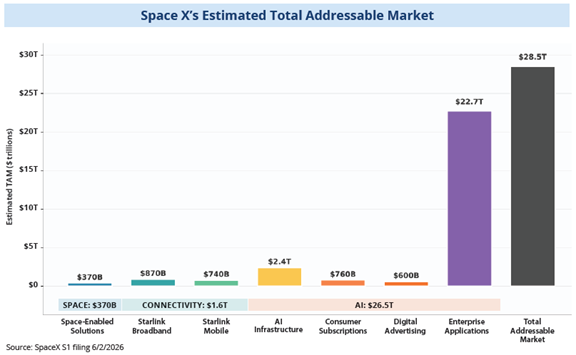

Evidence of unbridled exuberance is becoming increasingly common. SpaceX’s IPO debuted June 12th with the intention to raise $75 billion at a market capitalization of around $1.8 trillion, making it the largest IPO ever. The 24-year-old company generated about $18.7 billion in revenue last year, so at the IPO price, investors were buying shares at something around 100 times sales. It lost roughly $4.9 billion in 2025 after being profitable a year earlier, flipping into the red when it swallowed Elon Musk’s AI venture, xAI.

Yet despite the sizable loss, the future is bright in the eyes of investors thanks to stratospheric estimates for the artificial intelligence market. According to SpaceX’s S1 filing, over 90% of the company’s estimated total addressable market of $28.5 trillion will come from its AI-related businesses.

SpaceX is not the only blockbuster IPO anticipated this year. Anthropic said in early June that it had filed for an IPO, days after a private funding round valued the company at about $965 billion. The filing with the SEC was confidential, so details will be released nearer to the IPO, which could happen later this year.

Its direct competitor, OpenAI, has made its own confidential IPO filing. OpenAI’s valuation is expected to approach a trillion dollars based on its latest funding round, even as the ChatGPT creator may lose some $14 billion this year and expects no profit until around 2030.

Three of the largest IPOs in history could happen in succession. More importantly, all are competing in a new market with unsettled prospects and dynamics.

Priced with Certainty

The lofty growth assumptions embedded in these valuations assume the winners of the AI boom are already known with near certainty. These are the kinds of assumptions that legendary value investor Seth Klarman might take issue. In his book Margin of Safety, Klarman argued that a prudent buyer will demand an investment discount wide enough to try to account for the investment’s uncertainty. Competitive dynamics can change quickly, particularly in the technology sector. As Klarman put it, “Risk is not inherent in an investment; it is always relative to the price paid.”

Investors buying into the AI hype would argue the associated risk is being compensated with an asymmetric payoff potential. If AI turns out to be as transformative as its proponents expect, a stake in an eventual winner could return many times what it cost. The catch is that the payoff depends on market dynamics that have yet to be established. Specifically, the market for tokens.