Our investment team is closely monitoring the developments in the Middle East and the impact they are having on commodity prices, the stock market, and the world economy. We lament the loss of innocent life, pray for the safety of U.S. troops in harm’s way and mourn the U.S. military servicemembers who have lost their lives.

You will continue to hear from us on the conflict with Iran. In the meantime, if you have any questions on the markets and the economy or if there is anything we can do to support you and your clients during this difficult time, please reach out to us via our Investment Strategy Team’s email address at opsresearch@orion.com.

Weekly Notes from Tim

By Tim Holland, CFA, Chief Investment Officer

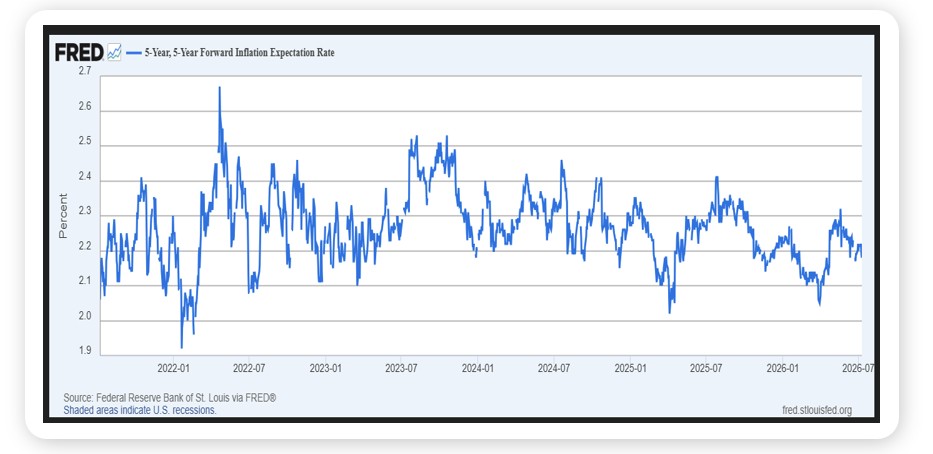

- When I think Great Expectations, I think of the Charles Dickens classic (and I think of Cheers, and Fraser trying to interest the bar in A Tale of Two Cities…if you need a laugh, I highly recommend the episode, it is brilliant). When I think Not So Great Expectations, I think of Wall Street’s expectations for what inflation will average over the five-year period beginning five years from now (which are not so great, which is a good thing).

- The Federal Reserve has a dual mandate – full employment and price stability. Sometimes the Fed is more focused on the labor market and sometimes the Fed is more focused on inflation. Today, with inflation running well above the Fed’s 2% target -- the Fed’s preferred inflation gauge, the Personal Consumption Expenditures Price Index recently came in at 4.1% -- and the US economy having put up better than expected job gains three of the last four months -- the Fed is very much focused on price stability, a point new Fed Chair Kevin Warsh emphasized during his first post-Fed meeting press conference in June (though in the spirit of full disclosure, the most recent jobs report came in well shy of expectations). Yet while the Fed is focused on price stability and has assumed a more hawkish footing, our central bank doesn’t seem to be in a rush to raise rates, nor is Wall Street clamoring for it to do so (investors are pricing in just one quarter point rate hike over the next year, and only marginally so), which brings us back to the focus of this week’s note, inflation expectations.

- While inflation is running well above the Fed’s 2% target, long-term inflation expectations remain, to use a favored Fed term, “anchored,” with Wall Street expecting inflation to average 2.18% over the five-year period beginning five years from now, essentially inline with pre-war readings and well off the post-pandemic high of 2.7% (see chart). And that’s a big deal…..if inflation and inflation expectations were both well above 2%, the Fed, we think, would have to raise rates; with expectations anchored, the Fed should have time to determine if the current spike in inflation, to use another, maybe less favored, Fed term, proves transitory. If the Fed doesn’t have to get back into the business of raising rates, our ongoing bull market should prove to be, well, ongoing.

Source, Federal Reserve Bank of St. Louis, July 2026

Looking Back, Looking Ahead

By Ben Vaske, CFA, Manager, Investment Strategy

Last Week

U.S. large cap growth stocks reasserted their dominance last week, with the S&P 500 gaining 1.3% and the NASDAQ 100 up 1.7%, while the Dow Jones, small caps, and value stocks all finished negative. International equities were mixed, with emerging markets the standout at 2.1% on the week, while developed markets were essentially flat. Emerging markets retain a commanding year-to-date lead at 22.5%, ahead of the NASDAQ 100 at 18.5%. Commodities were the week's standout among broader asset classes, rising 3.2%, while the Bloomberg Agg edged down 0.4% as the 10-year Treasury yield climbed back firmly above 4.5%.

The Fed minutes from Kevin Warsh's first FOMC meeting were released Wednesday and painted a picture of a deeply split committee, with half of members projecting a rate hike by year-end, higher inflation forecasts baked in, and disclosures that were intentionally less informative than prior releases. The broader read on Warsh, however, suggests his focus may center more on reforming Fed communications and balance sheet policy than on aggressive rate action, a meaningful recalibration from what markets had been pricing. Separately, consumer credit posted its first monthly decline since November 2024, led by a sharp drop in revolving credit, adding to questions about the durability of consumer spending as the economy's primary growth engine.

This Week

It is a heavy week on both the economic and earnings calendars. CPI is due Tuesday and is projected to decline to 3.8% from last month's 4.2% reading, which would be a welcome development for markets and the Fed alike. PPI follows Wednesday and retail sales Thursday. On the earnings front, Q2 season kicks off in earnest with several major financial institutions reporting alongside Netflix and UnitedHealth. Early results from the 4% of S&P 500 companies that have already reported show 89% beating EPS estimates, and full-quarter growth is currently tracking at 23.6% year-over-year, which would mark the second consecutive quarter above 20%.

We hope you have a great week. If there’s anything we can do to help you, please feel free to reach out to ben.vaske@orion.com or opsresearch@orion.com.