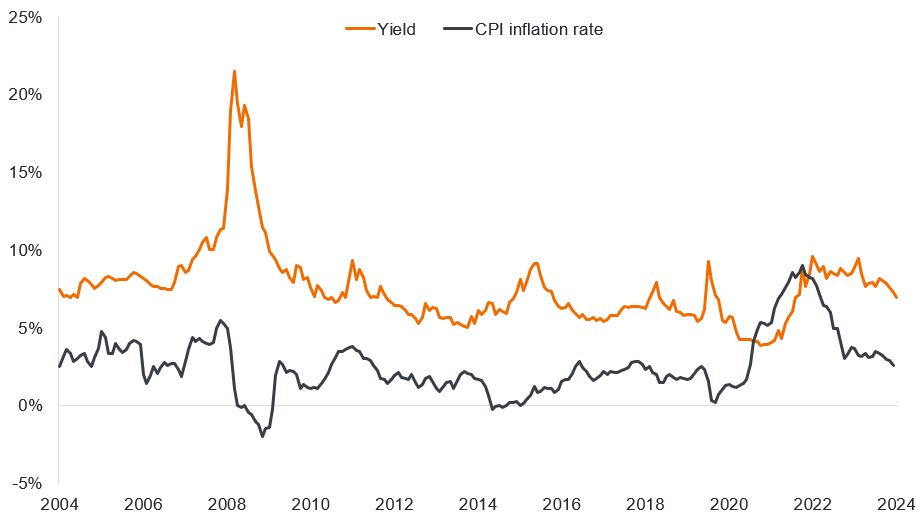

A common refrain amongst the investment community is that with central banks moving to cut rates, inflation must be tamed and economic strength is the new concern. In such an environment, it makes sense to move up in quality within corporate bonds because you will be more exposed to bonds that are more interest rate sensitive and less exposed to credit sensitive assets.

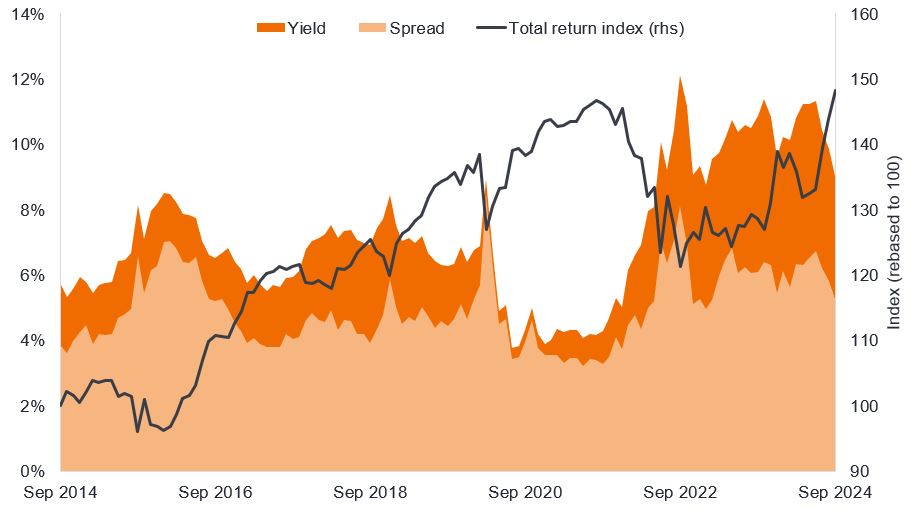

We do not disagree with the central premise of this argument. Where we think it falls down is when it is applied simplistically. One could quite easily have assembled a convincing case for an impending recession in the past 24 months – inverted yield curves, weak purchasing manager indices, subdued consumer confidence – and avoided high yield bonds in their entirety. To do so would have been costly as global high yield bonds, represented by the ICE Global High Yield Bond Index, delivered a total return in US dollars of 31.9% over the 24 months to 30 September 2024.1