Resilient Portfolios Have Worked · Emerging Markets Beyond China · What Is Dr. Copper’s Diagnosis?

Portfolio Advice, Talking Points, and Useful Resources

- Resilient portfolios empower investors to participate in the global economy and financial markets’ growth while dampening losses during equity bear markets.

- Emerging markets continue to have attractive relative valuations, but India presents an intriguing growth story.

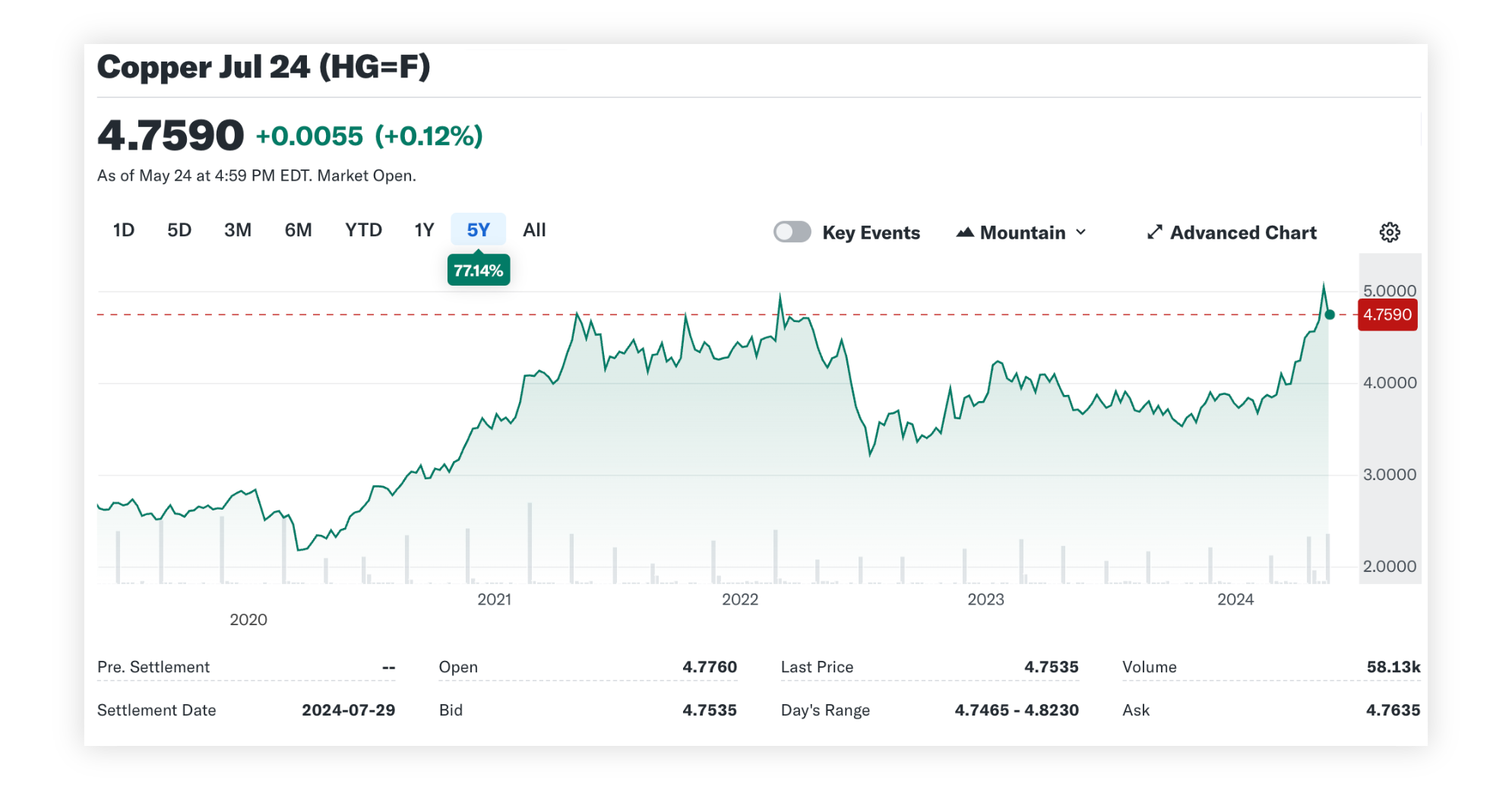

- Prices for copper, which is often considered a leading indicator of the global economy, have surged.

Halfway through the second quarter, the stock market continues to enjoy a positive start to the year. As of this writing, U.S. benchmarks are on five-week winning streaks and the stock market has recovered its recent losses while moving to new highs. Not only are U.S. stocks performing well, but non-U.S. stocks, including emerging markets, and commodities such as copper are also showing strength. Diversifying asset classes, such as global credit, alternatives, and real assets, also continue to help diversify equity-dominated investment portfolios. However, core fixed income continues to be mired in a multi-year bear market.

In this report, we’ll discuss why staying the course with resilient, global, multi-asset portfolios makes sense. We’ll also review emerging markets and one commodity market that might be sending an important signal for the global economy.

Resilient Diversified Portfolios Have Worked

There is a notion that diversified portfolios have failed in recent years. I disagree.

Globally diversified portfolios have worked. Sure, the TV benchmarks, such as S&P 500, Nasdaq and Dow Jones Industrials, have generated above-average returns in recent years. But compared to their long-term historical experience, the recent performance of globally diversified portfolios has been solid. Looking forward, globally diversified portfolios seem positioned to continue delivering strong results. Considering investors invest to participate in the long-term growth of the economy and markets but also need to build in portfolio resilience to stay the course during market stress (or the anxiety of potential stress), globally diversified, multi-asset portfolios have succeeded in recent years.

First, let’s look at the historical experience. For this exercise, we’ll review a simple, traditional U.S.-based balanced portfolio and compare it to a more globally diversified, multi-asset portfolio that incorporates non-U.S. stocks and diversifying asset classes. Using the Global Investment Returns Yearbook 2024 from UBS Global as a source for long-term historical returns, plus factoring in the U.S. inflation rate since 1974 of 3.8%, the classic U.S.-based 60% equities (S&P 500 large-cap equities) and 40% fixed income (Bloomberg Aggregate Bond Index) portfolio has returned ~9% per year since 1974. Meanwhile, the real return for a global, balanced portfolio of 60% equities and 40% fixed income has been about 0.8% lower per year than its U.S.-only balanced counterpart.

Over the last five years, through mid-May 2024, the U.S.-based 60/40 has returned ~9%. Essentially, that matches the 50-year average. Meanwhile, the globally diversified, multi-asset portfolio returned ~8%. Again, basically in the ballpark of its 50-year average. (For the purposes of this exercise, for the global, multi-asset portfolio, the portfolio weights used were 60% equities and 40% diversifiers. The equity portion consisted of 60% U.S.-based and 40% international. The diversifying 40% segment was split between core fixed income (U.S. investment-grade bonds and cash) and diversifying asset classes equally allocated between global credit (high yield), alternatives, and real assets (commodities).

It’s clear that investors want to participate in the upside of stock market growth but lose less on the downside. In 2022, during the last bear market in the U.S., the S&P 500 lost 18%. The U.S.-based balanced portfolio, meanwhile, lost 16%. The globally diversified, multi-asset portfolio lost 13%.

Moving forward, what might investors expect? Here, an interactive tool that is free to the public — Asset Allocation Interactive from Research Affiliates — provides useful insight. Research Affiliates uses current valuations and yields to forecast forward nominal returns, which it predicts will be higher for all asset classes, except for U.S. large-caps and commodities. Thus, even with elevated valuations in the U.S., globally diversified, multi-asset portfolios should generate premium returns to cash and inflation.

Emerging Markets Beyond China

Emerging markets have large, young populations and fast-growing economies, which are driving consumption. These markets are home to 85% of the world’s population. That’s 5.6x the rest of the world. Emerging markets also have 8.8x the number of young people under the age of 30 than rest of the world and 35% of the world’s consumers, as of 2010. In 2025, that number is expected to have grown to 53%. As McKinsey & Company stated in its report “Winning the $30 Trillion Decathlon,” the growth of emerging market consumers is “the biggest growth opportunity in the history of capitalism.”

Of course, one problem with emerging markets is state-owned enterprises (SOEs), which are companies owned and controlled by governments. These companies have conflicts of interest, poor corporate governance and widespread corruption, and they are inefficient. The largest emerging market ETFs, for instance, have ~30% in SOEs.

The Chinese stock market is often synonymous with emerging market investing. That’s for good reason, as China has had the world’s largest population and historically some of the greatest economic growth. But it also has significant government interference. In turn, China’s weight in the emerging market indices has dropped considerably in recent years. The beneficiary is India. India has very attractive qualities. It will soon have the largest population in the world. It is already larger than all the other emerging market countries, excluding China, combined. And India already has more young people than China and the U.S. combined! These population numbers show up in economic growth, too. While the U.S. is projecting GDP growth of 2.1% in 2024, according to the IMF, China is expected to grow 4.6%. Emerging markets overall are predicted to grow at 4.1%, and India’s expected GDP growth in 2024 is 6.5%. While much has been made about the loss of the middle class in the U.S., the middle class in India has grown from 30% of the Indian population in 2005 to an expected 78% in 2030. This translates into consumption that already matches China’s and is expected to double over the next 20-plus years.

And there’s more. India has unmatched human capital: world-class tech schools, a tech ecosystem that is more than 50 years old, surging infrastructure spending, and the world’s most popular leader, Prime Minister Narendra Modi.

A potential problem with the Indian market is valuations. They are even higher than the U.S.’s. But, if one considers those valuations versus growth prospects, India becomes much more reasonable. India’s valuation/growth ratios are nearly 40% lower than the U.S.’s, although they are not as low as emerging markets in general nor China, whose current ratios are 65% lower than the U.S.’s.

Even though emerging markets, especially China, have underperformed in recent years, opportunity in this asset class remains. It is not just a valuation story, but a growth story.

How should investors consider sizing a position in emerging markets? For a frame of reference, emerging markets currently make up 7% of the global equity market, as represented by the ETF ACWI, which includes both U.S. and non-U.S. equities. But emerging markets make up 50% of the world’s GDP and have contributed 66% of the world’s GDP growth over the last 10 years. China makes up about 3% of the global stock market and 19% of global GDP, while India makes up about 2% and has contributed 10% of global GDP.